How Jeffrey Epstein Avoided Paying Taxes On His Properties: A Deep Dive Into Tax Loopholes

Have you ever wondered how wealthy individuals like Jeffrey Epstein managed to avoid paying taxes on their extensive property holdings? The case of Jeffrey Epstein's tax-free properties raises important questions about wealth inequality, tax loopholes, and the fairness of our tax system. How did someone with billions in assets manage to legally sidestep millions in tax obligations that ordinary citizens cannot avoid?

This article examines the controversial tax strategies employed by Jeffrey Epstein, exploring the legal mechanisms that allowed him to maintain luxury properties while paying little to no property taxes. We'll uncover the complex world of tax shelters, offshore entities, and legal loopholes that enabled this tax avoidance, while also considering the broader implications for our tax system and society.

Jeffrey Epstein: A Brief Biography

Jeffrey Epstein was a financier and convicted sex offender who built a vast network of wealth and influence before his death in 2019. Born in 1953 in Brooklyn, New York, Epstein worked as a teacher before moving into finance, eventually founding his own wealth management firm.

Personal Details and Bio Data

| Detail | Information |

|---|---|

| Full Name | Jeffrey Edward Epstein |

| Date of Birth | January 20, 1953 |

| Place of Birth | Brooklyn, New York, USA |

| Date of Death | August 10, 2019 |

| Occupation | Financier, Registered Sex Offender |

| Education | Cooper Union (dropped out), Courant Institute of Mathematical Sciences at NYU (attended) |

| Net Worth | Estimated $500 million - $1 billion (at time of death) |

| Known For | Financial wealth, connections to powerful individuals, sex trafficking conviction |

Understanding Property Tax Loopholes: How the Wealthy Avoid Taxes

Property tax avoidance isn't unique to Jeffrey Epstein, though his case gained significant attention due to his high profile. The wealthy have long utilized various legal strategies to minimize their tax obligations, and understanding these methods is crucial to comprehending how someone could own multiple luxury properties while paying minimal taxes.

The Mechanics of Property Tax Avoidance

Property taxes are typically assessed based on the value of real estate owned. However, several strategies can reduce or eliminate these obligations:

1. Non-profit or Religious Exemptions: Properties designated for non-profit or religious use may qualify for tax exemptions. Epstein allegedly used this strategy by creating entities that appeared to serve charitable purposes.

2. Agricultural Designations: Some wealthy property owners have reclassified their land as agricultural to benefit from lower tax rates. This involves meeting minimal requirements to qualify for agricultural tax breaks.

3. Offshore Holdings: By placing properties in offshore trusts or corporations, owners can create layers of legal entities that complicate tax assessment and collection.

4. Conservation Easements: Donating development rights to conservation organizations can provide significant tax deductions while maintaining ownership of the property.

Jeffrey Epstein's Tax-Free Properties: The Specifics

Epstein's property portfolio included multiple high-value assets across the United States and abroad. His primary residence in New York City, a massive townhouse on the Upper East Side, became a focal point of tax controversy.

The New York Townhouse Controversy

Epstein's Manhattan townhouse, valued at approximately $56 million, was reportedly classified under a tax-exempt status linked to a foundation he established. This classification allowed him to avoid paying millions in property taxes that would typically apply to such a valuable property.

The property was allegedly tied to a foundation named after his younger brother, Mark Epstein. This foundation was purportedly created for charitable purposes, which would qualify it for tax-exempt status under certain conditions. However, questions arose about whether the property was genuinely being used for charitable activities or merely serving as a tax shelter.

Other Properties and Tax Strategies

Beyond his New York residence, Epstein owned properties in:

- Palm Beach, Florida

- U.S. Virgin Islands (Little Saint James Island)

- New Mexico (Zorro Ranch)

- Paris, France

- The Netherlands

Each of these properties potentially utilized different tax avoidance strategies based on local laws and regulations. In some cases, properties were held through complex corporate structures that obscured true ownership and made tax assessment more difficult.

The Legal Framework: How Tax Loopholes Exist

The ability of wealthy individuals to avoid property taxes isn't simply a matter of clever accounting—it's built into the legal framework of our tax system. Understanding this framework helps explain how such strategies are possible.

Tax Code Complexity

The U.S. tax code contains over 70,000 pages of regulations, many of which include provisions that benefit specific types of property ownership or organizational structures. These provisions often originated with legitimate purposes but have been exploited for tax avoidance.

Key factors that enable tax avoidance include:

- Vagueness in tax law: Many tax regulations contain ambiguous language that can be interpreted in multiple ways

- Jurisdictional differences: Property tax laws vary significantly between states and municipalities

- Loophole exploitation: Wealthy individuals can afford specialized legal counsel to identify and exploit tax loopholes

- Offshore jurisdictions: Some countries offer favorable tax treatment to attract foreign investment

The Role of Professional Advisors

Wealthy individuals like Epstein typically employ teams of attorneys, accountants, and financial advisors who specialize in tax optimization. These professionals identify legal strategies to minimize tax obligations, often pushing the boundaries of what's considered ethical.

Ethical Implications: Is Tax Avoidance Fair?

The case of Jeffrey Epstein's tax-free properties raises profound ethical questions about wealth inequality and tax fairness. While his strategies may have been legal, they highlight systemic issues in our tax system.

The Impact on Public Services

When wealthy individuals avoid paying their fair share of property taxes, the burden shifts to middle and lower-income property owners. This can result in:

- Reduced funding for schools: Property taxes often fund local education systems

- Infrastructure deterioration: Less tax revenue means less money for roads, bridges, and public facilities

- Increased tax rates for others: To compensate for lost revenue, tax authorities may raise rates on other properties

The Social Contract Debate

The ability of the wealthy to avoid taxes raises questions about the social contract—the implicit agreement that citizens will contribute to society based on their ability to pay. When billionaires pay little to no property taxes while owning multiple luxury properties, it challenges the fairness of this system.

Similar Cases: Other Wealthy Individuals and Tax Avoidance

Jeffrey Epstein isn't alone in utilizing tax avoidance strategies. Numerous other wealthy individuals and corporations have faced scrutiny for similar practices.

Notable Examples

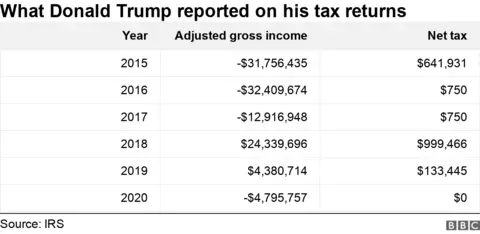

Donald Trump: The former president famously paid only $750 in federal income taxes in 2016 and 2017, according to a New York Times investigation. His tax strategies included claiming massive business losses to offset income.

Amazon: In 2019, the retail giant paid $0 in federal income taxes despite earning billions in profits, utilizing various tax credits and deductions.

ProPublica Investigations: Recent reporting has revealed how billionaires like Elon Musk, Warren Buffett, and Jeff Bezos pay relatively little in income taxes compared to their wealth accumulation.

Legal vs. Ethical: Where Should the Line Be Drawn?

The distinction between legal tax avoidance and illegal tax evasion is crucial but often blurry. While Epstein's property tax strategies may have been technically legal, they raise questions about where the ethical line should be drawn.

The Difference Between Avoidance and Evasion

Tax avoidance involves using legal methods to minimize tax obligations, while tax evasion involves illegal practices like underreporting income or claiming false deductions. The wealthy often operate in the gray area between these two concepts.

Proposed Reforms

To address these issues, various tax reform proposals have been suggested:

- Closing loopholes: Eliminating specific provisions that enable tax avoidance

- Increasing transparency: Requiring greater disclosure of ownership structures

- Implementing wealth taxes: Taxing net worth rather than just income and property

- International cooperation: Coordinating tax policies across jurisdictions to prevent offshore tax sheltering

The Broader Context: Wealth Inequality in America

The ability of individuals like Jeffrey Epstein to avoid property taxes exists within the broader context of growing wealth inequality in the United States.

Statistics on Wealth Concentration

- The top 1% of Americans own 40% of the country's wealth

- The wealthiest 400 Americans own more wealth than the bottom 150 million combined

- The wealth gap between the richest and poorest Americans has widened significantly over the past 40 years

This concentration of wealth enables the ultra-rich to invest in sophisticated tax avoidance strategies that are unavailable to average citizens.

Conclusion: Reforming the System

The case of Jeffrey Epstein's tax-free properties illuminates the complex relationship between wealth, power, and the tax system. While his specific strategies may have been legal, they highlight fundamental inequities in how property taxes are assessed and collected.

Key takeaways from this analysis include:

- Wealthy individuals can legally avoid millions in property taxes through various strategies

- The tax code's complexity enables sophisticated avoidance techniques

- These practices shift the tax burden to middle and lower-income property owners

- Reform proposals range from closing loopholes to implementing wealth taxes

- The broader issue connects to systemic wealth inequality in America

As we consider tax reform, it's essential to balance the need for revenue with the desire to create a fair system that doesn't unduly burden any particular group. The controversy surrounding Jeffrey Epstein's properties serves as a stark reminder that our current system allows the ultra-wealthy to benefit from public services without contributing their fair share to support them.

The question remains: will we continue to allow such tax avoidance, or will we work toward a more equitable system that ensures everyone pays their fair share based on their ability to contribute?