What Is A Billing Address? Your Complete Guide To Understanding, Using, And Protecting It

Have you ever been checking out online, cart full of goodies, only to be stopped dead in your tracks by a field labeled "Billing Address"? You type in your shipping info, but now this? What is a billing address, really? Is it the same as where your packages go? Why does every website from Amazon to your local utility company demand it? If you've ever felt a moment of confusion staring at that form, you're not alone. This seemingly simple string of words—your street, city, zip code—holds immense power in the digital and financial worlds. It's the silent guardian of your transactions, a key piece of your financial identity, and a critical tool for businesses. This guide will dismantle the mystery once and for all. We'll explore exactly what a billing address is, why it's non-negotiable for modern commerce, how it differs from your shipping address, and the vital security role it plays. By the end, you'll not only know the answer but also understand how to use this information wisely to protect yourself and streamline your online life.

The Core Definition: What Exactly Is a Billing Address?

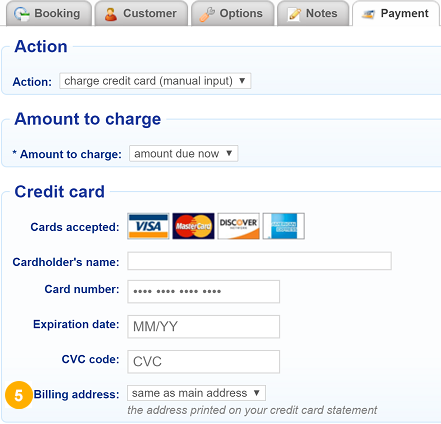

At its most fundamental, a billing address is the specific street address associated with a primary payment method, most commonly a credit or debit card. It is the official location on file with the bank or financial institution that issued your card. Think of it as your payment method's "home address." When you make a purchase, especially online or over the phone, the billing address you provide is used as a verification tool. The merchant's payment processor checks the address you enter against the address the bank has on file. A match is a strong signal that the person using the card is the legitimate cardholder.

This process is part of a broader security system called Address Verification Service (AVS). AVS is a fraud-prevention tool used primarily in the United States, Canada, and the United Kingdom. When you enter your billing address during a transaction, the system compares the numeric portion (street number and zip/postal code) with the issuer's records. A "full match" means both the street number and zip code align. A "partial match" might mean only the zip code matches. A "no match" or "address unavailable" can trigger a red flag, potentially causing the transaction to be declined for security reasons. It's crucial to understand that the billing address is tied to the payment instrument, not necessarily to the physical location where you are making the purchase.

Breaking Down the Components: What Makes Up a Billing Address?

A standard billing address in the U.S. follows a specific format that leaves no room for ambiguity. Each component serves a precise purpose for mail delivery and, crucially, for database matching. The typical structure includes:

- Recipient Name: This is the name of the account holder as it appears on the financial account. For individuals, it's your legal first and last name. For businesses, it's the official business name.

- Street Address: This is the core component. It includes the specific building number, street name, and any apartment, suite, or unit number (e.g., "123 Main St, Apt 4B"). Accuracy here is paramount for AVS.

- City: The city name corresponding to the street address.

- State: The two-letter postal abbreviation (e.g., CA, NY, TX).

- ZIP Code: The five-digit (or ZIP+4) postal code. This is often the most heavily weighted part of the AVS check. An incorrect ZIP code is a frequent cause of transaction failures.

- Country: For international transactions, the full country name is required.

When filling out a form, it's vital to enter this information exactly as it appears on your bank statement or online banking profile. This includes using standard abbreviations (like "St" for Street, "Ave" for Avenue) and ensuring no extra spaces or punctuation that aren't on file. A minor typo in the street number or a missing apartment number can lead to a failed verification.

Why Is Your Billing Address So Important? The Dual Role

The billing address isn't just bureaucratic busywork; it serves two critical, interconnected functions in the financial ecosystem: fraud prevention and transaction authorization.

The First Line of Defense: Fraud Prevention

In an era of data breaches and sophisticated cybercrime, the billing address is a cornerstone of card-not-present (CNP) fraud prevention. CNP transactions—those made online, via phone, or by mail—are inherently riskier than swiping a card at a physical store because the merchant cannot see the card or the cardholder. The billing address acts as a shared secret between you and your bank. A fraudster who has stolen your card number from a compromised database likely does not have your exact billing address. When they attempt a purchase, the AVS check will fail, alerting the merchant's system and often leading to an automatic decline. According to industry reports, CNP fraud accounts for a significant and growing portion of all card fraud, making tools like AVS more important than ever. It creates a significant hurdle for criminals, protecting both consumers and merchants from unauthorized charges.

The Key to Authorization: Proving "You" Are You

Beyond stopping bad actors, the billing address is a fundamental requirement for the authorization process. When you click "Place Order," your transaction details are encrypted and sent to your card issuer via the payment gateway. The issuer must decide: "Is this a valid transaction from the legitimate cardholder?" The billing address match is a primary data point in this decision. A successful AVS match increases the likelihood of authorization. A failed match can result in:

- An immediate decline.

- A request for additional verification (like a one-time password sent to your phone).

- The transaction being flagged for manual review by the fraud department, causing significant delay.

For recurring payments—subscriptions to Netflix, Spotify, or monthly software services—the billing address is verified once during setup. If it ever becomes invalid or doesn't match (e.g., you moved and updated your shipping address but forgot your bank), the recurring payment can fail, leading to service interruptions. This is why subscription management platforms always ask for and verify a billing address.

Billing Address vs. Shipping Address: Clearing Up the Confusion

This is the most common point of confusion, and understanding the difference is crucial. While they can be the same, they serve entirely different purposes.

| Feature | Billing Address | Shipping Address |

|---|---|---|

| Primary Purpose | Financial Verification & Authorization | Physical Delivery of Goods |

| Linked To | Your payment method (credit/debit card) | Your order and the logistics network |

| Verification System | Address Verification Service (AVS) by the bank | Carrier logistics (USPS, UPS, FedEx) |

| What Happens if Wrong? | Transaction is declined or flagged for fraud. Payment fails. | Package is misdelivered, delayed, or returned. Goods don't arrive. |

| Can They Differ? | Yes, absolutely. Common for gifts, business purchases, or if you use a PO Box for billing. | Yes. This is the whole point of having two separate fields. |

Practical Example: You live in New York (your billing address on your Amex card) but are buying a birthday gift for your mom in California. You will enter your New York address in the "Billing Address" field and your mom's California address in the "Shipping Address" field. The payment will be authorized based on your NY address, and the package will be sent to CA. This is a perfectly normal and valid transaction.

When They Must Match: Some merchants, particularly for high-risk items or digital goods, may have policies requiring the billing and shipping addresses to match to mitigate fraud. This is more common with certain financial services or high-value electronics. Always check the merchant's terms if you encounter this requirement.

The Security Backbone: How Your Billing Address Protects You

We've touched on AVS, but the billing address is part of a larger security tapestry. It works in concert with other data points to create a robust authentication profile.

- The "Something You Have" Factor: Your physical card (or its digital representation in a wallet like Apple Pay) is "something you have." The billing address linked to it is "something you know" (or more accurately, something the bank has on file that you must correctly replicate). This two-factor concept strengthens security.

- Geolocation and IP Address: Modern fraud systems don't just check AVS. They also analyze the IP address of the device making the purchase. If your transaction originates from a IP geolocated in another country while your billing address is in the U.S., it raises the risk score. A match between IP geolocation and billing address country is a positive signal.

- The 3-D Secure Protocol: You've likely seen this as "Verified by Visa" or "Mastercard SecureCode." When triggered, it redirects you to your bank's page to enter a password or a one-time code. Your billing address information is often pre-populated or used as part of this secondary authentication step, confirming your identity beyond the initial AVS check.

Your Actionable Security Tip: Never share your full billing address unnecessarily. Only provide it on secure, trusted websites (look for "https://" and a padlock icon in the address bar). Be wary of phishing emails or phone calls asking to "verify" your billing address—your bank will never ask for it in full via these channels.

Common Billing Address Mistakes That Cause Transaction Failures

Even a small error can derail a payment. Here are the most frequent pitfalls:

- Using an Old Address: This is the #1 culprit. If you moved six months ago and updated your shipping address with Amazon but not your bank, your card's billing address is still the old one. Solution: The moment you move, update your billing address with every financial institution where you have a credit card, debit card, or loan. This includes your primary bank, credit card companies, and even PayPal or Venmo.

- Abbreviation Inconsistency: Your bank might have "Street" on file, but you type "St." Or they have "Avenue" and you use "Ave." While systems are getting smarter, some are strict. Solution: Look at a recent paper statement from the bank. Copy the address format exactly.

- Omitting Apartment/Suite Numbers: If your address includes a unit, and you leave it blank, the AVS system may see a mismatch between "123 Main St" (your entry) and "123 Main St, Apt 5" (their file). Solution: Always include unit numbers, using standard abbreviations like "Apt," "Ste," "Unit," or "#".

- Confusing Billing and Shipping: Rushing through checkout and pasting your shipping address into the billing field. Solution: Slow down. Use a password manager that can store multiple addresses, or keep your correct billing address saved in a secure note for copy-paste.

- International Address Formatting: Non-U.S. addresses have different structures (e.g., postal code before city in the UK). Solution: When in doubt, follow the format prompts on the payment form. They are usually tailored for the country of the card issuer.

Special Cases: PO Boxes, Virtual Addresses, and Business Accounts

- Can I Use a PO Box as a Billing Address?Generally, no. Banks and most credit card issuers require a physical street address for billing because AVS systems are designed to verify physical locations, not PO boxes. A PO Box is typically acceptable for a shipping address but will fail AVS for the billing address. Some premium banking services or specific card products for businesses with mail-forwarding services might allow exceptions, but it's not the norm for consumer cards.

- What About a Virtual Mailbox or UPS Store Address? Similar to a PO Box, these are commercial mail receiving agencies (CMRAs). While they provide a real street address, many AVS systems are configured to flag or reject addresses known to be CMRA locations (like "123 Main St, UPS Store #456") because they are not unique residential or business physical locations. It's risky and often unsuccessful.

- Business Credit Cards: The billing address is typically the official headquarters or principal place of business of the company as registered with the issuer and on the business's legal documents (like articles of incorporation). The individual employee's name may be on the card, but the address is the corporate one.

The Future of the Billing Address: Are We Moving Away From It?

With the rise of digital wallets (Apple Pay, Google Pay, Samsung Pay) and tokenization, the traditional act of typing a billing address is becoming less common for the everyday consumer. When you use Apple Pay, your device shares a unique, encrypted device-specific token with the merchant, not your actual card number. The billing address verification often happens behind the scenes during the initial card setup in the wallet, where you did have to provide it. However, the underlying need for that verification hasn't disappeared; it's just been shifted to the enrollment phase. For merchants without digital wallet support or for certain high-value transactions, the manual entry of a billing address remains a standard and necessary security layer. It is deeply embedded in the global financial infrastructure and is unlikely to vanish entirely in the foreseeable future.

Conclusion: Your Billing Address Is More Than a Form Field

So, what is a billing address? It's far more than a mundane line on a checkout form. It is your financial anchor, a critical piece of your payment identity that acts as a first responder in the fight against fraud. It is the silent gatekeeper that determines whether your transaction sails through or gets stuck in limbo. Understanding its purpose—that it belongs to your card, not your cart—empowers you to navigate online commerce with confidence and security.

The takeaway is simple but powerful: Treat your billing address with the same care you treat your card number and PIN. Keep it updated with your bank. Enter it meticulously and exactly as on file. Recognize that when a site asks for it, they are performing a vital security check, not just collecting data. By mastering this small but mighty piece of information, you protect your finances, ensure your purchases go smoothly, and become a smarter, more secure participant in our digital economy. The next time you see that field, you won't see a hurdle—you'll see a shield, and you'll know exactly how to wield it.