C6 Z06 For Sale With A 180-Month Finance Term: Is A 15-Year Car Loan Ever A Smart Move?

What if you could drive home a supercar-level machine like the Corvette C6 Z06 for a monthly payment that feels like a family sedan? That’s the tantalizing, and frankly controversial, promise of a 180-month (15-year) auto loan. It’s a term that makes traditional car buyers shudder, yet it’s increasingly discussed in forums and by some lenders for high-ticket vehicles. If you’ve found a C6 Z06 for sale and are staring at a 180-month finance option, your head is probably spinning with questions. Is this a golden ticket to owning a legendary American sports car, or a fast track to financial ruin? This comprehensive guide will dissect the 180-month term for the C6 Z06, exploring the mechanics, the massive risks, the rare scenarios where it might make sense, and the smarter alternatives you should consider first.

Understanding the Beast: The Chevrolet Corvette C6 Z06

Before we dive into the labyrinth of long-term financing, we need to understand the star of the show. The C6 generation Corvette (2005-2013) represented a bold, modern evolution of America’s sports car. Within this generation, the Z06 model (introduced in 2006) was the track-focused, high-performance flagship.

The Legendary LS7 Engine and Performance Credentials

The heart of the C6 Z06 is its 7.0-liter LS7 V8 engine, a naturally aspirated masterpiece that produced 505 horsepower and 470 lb-ft of torque. This was, and remains, an astonishing specific output for a pushrod engine. Paired with a robust 6-speed manual transmission (or a 6-speed automatic for later models), the Z06 could rocket from 0-60 mph in under 3.7 seconds and conquer the quarter-mile in the mid-11-second range. Its top speed was electronically limited to 198 mph.

Key performance features that define the C6 Z06 include:

- Aluminum Frame: The Z06 used a lightweight aluminum spaceframe, saving significant weight over the standard steel frame.

- Wider Stance: It featured wider rear bodywork and larger tires to handle the extra power.

- Enhanced Braking: Massive 14-inch cross-drilled rotors with 6-piston calipers in the front and 14-inch rotors with 4-piston calipers in the rear provided immense stopping power.

- Suspension Tuning: Magnetic Selective Ride Control (MSRC) was available, offering adaptive damping that was revolutionary for its time.

The C6 Z06 as a Modern Classic and Investment

Today, the C6 Z06 occupies a unique space. It’s old enough to be considered a modern classic, with design cues that are now iconic, yet new enough (2006-2013 models) that many are still relatively reliable and parts are available. Its value trajectory has been interesting. While not appreciating like some ultra-rare exotics, clean, low-mileage examples, particularly 2008-2013 models with the LS7, have seen steady price increases. It’s a driver’s car first and an investment second, but one that holds its value better than most performance cars of its era. This residual value is a critical, yet often overlooked, factor when considering a long-term loan.

The 180-Month (15-Year) Finance Term: Anatomy of an Unusual Loan

A 180-month term is exceptionally long for any vehicle. The standard new car loan is 60-72 months. Even used car loans rarely exceed 84 months. So why does this term exist, and what does it actually do?

How a 180-Month Term Drastically Lowers Your Monthly Payment

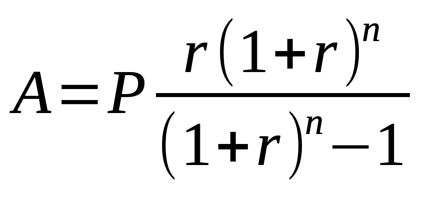

The primary, and often only, appeal of a 180-month term is the monthly payment shock absorber. Let’s use a concrete example. Assume a C6 Z06 with a sale price of $45,000, a 10% down payment ($4,500), and a 7% interest rate (typical for a used performance car with average credit on a long term).

- On a 72-month (6-year) loan: Your principal is $40,500. The monthly payment would be approximately $665.

- On a 180-month (15-year) loan: The same principal. The monthly payment plummets to approximately $361.

That’s a $304 per month difference. For someone budget-conscious but dreaming of a Z06, that number is intoxicating. It transforms an unattainable car into a seemingly manageable monthly expense. This is the siren song of the long-term loan: affordability today.

The Devastating Cost of “Affordability”: Interest and Negative Equity

But that lower payment comes at a catastrophic cost. Let’s calculate the total price paid for that $40,500 loan at 7%:

- 72-month loan total paid: ~$47,880 (Interest: ~$7,380)

- 180-month loan total paid: ~$64,980 (Interest: ~$24,480)

You would pay over $17,000 more in interest alone with the 15-year term. That’s enough to buy a decent used daily driver outright. You are essentially financing the car two or even three times over its realistic useful life.

The second, more insidious problem is negative equity or being “upside-down” on the loan. Cars depreciate fastest in the first few years. A C6 Z06, while holding value well, still loses a significant portion of its value in the first 3-5 years. With a 180-month loan, your principal balance will decline at a glacial pace. For the first 4-5 years of the loan, you will owe far more on the loan than the car is worth. If the car is totaled or stolen, your insurance will pay the actual cash value, not what you owe. You would be on the hook for thousands of dollars to settle the loan. If you need to sell the car due to a life change, you must write a check to the bank to do so.

Is a 180-Month Term on a C6 Z06 Ever Justifiable? The Niche Scenarios

While we’ve been heavily critical, there are a few narrow, high-specificity scenarios where this structure could be a calculated tool, not a trap. These are exceptions, not the rule.

Scenario 1: The “Cash-Flow Bridge” for a Strategic Buyer

Imagine a buyer with excellent credit who secures a very low interest rate (e.g., 3-4%) on a 180-month term from a credit union or specialty lender. They take the low payment but aggressively pay extra principal every single month, effectively treating it as a 5- or 6-year loan with a safety net. The long term acts as a payment floor. If a month is tight, they pay the minimum. If they have surplus cash, they pay down the principal aggressively, drastically cutting the total interest paid and the loan term. This requires immense discipline and a solid income. The key is the low rate—the 7% example above makes this strategy impossible.

Scenario 2: The “Hold Forever” Enthusiast with No Other Debt

This is a person who plans to keep this specific C6 Z06 for 15+ years until it’s a classic. They have no other debt, a massive emergency fund, and the car is their only financed asset. They view the total interest paid as the “cost of entry” to use their capital for other investments (like a retirement account) that they believe will yield a higher return than the loan’s interest rate. This is a sophisticated financial bet that hinges on their investment performance and their unwavering commitment to one car for a decade and a half. It also assumes the car remains reliable and desirable that long.

Scenario 3: The “Credit Rebuilder” with No Other Options

Someone with severely damaged credit may only qualify for long-term, high-interest loans. A 180-month term might be the only way a lender will approve them for the loan amount. In this case, the goal isn’t the car—it’s the positive payment history. Making every payment on time for 15 years would be a powerful credit repair tool. However, the astronomical interest paid (often 15%+) makes this a brutally expensive form of credit building. A secured credit card or a credit-builder loan would be far cheaper and less risky paths to rebuild credit.

The Smarter Path: Alternatives to a 180-Month Loan for a C6 Z06

If your goal is to own a C6 Z06 without financial suicide, here are the strategies that actually work.

1. The 60-72 Month “Traditional” Loan with a Large Down Payment

This is the gold standard. Aim for a 72-month loan at most. Your goal should be to put at least 20% down. On a $45,000 Z06, that’s a $9,000 down payment. This achieves three things:

- It lowers your monthly payment.

- It keeps you right-side-up on the loan from day one (or very close to it).

- It reduces the total interest paid dramatically.

- It gets you better interest rates from lenders.

2. The “Bank Yourself” Strategy: Save and Pay Cash

This is the ultimate financial win. The C6 Z06 market has cooled from its pandemic peak. Prices for driver-quality examples are more reasonable. Instead of financing, treat the car as a savings goal. Open a separate high-yield savings account. Automate a monthly transfer. In 24-36 months, you can walk into a “C6 Z06 for sale” transaction as a cash buyer. You’ll get a better price (no financing markup for the seller), pay zero interest, and own an asset free and clear. The discipline required is high, but the financial freedom is absolute.

3. The “Loan Refinance” Gamble

If you already have a predatory long-term loan, your escape hatch is refinancing. After 12-24 months of on-time payments, your credit may have improved, and you may have paid down enough principal to refinance the remaining balance into a shorter-term loan (48-60 months) at a lower rate. This will increase your monthly payment but will save you tens of thousands in future interest and get you out of the loan years sooner. This is a damage-control strategy, not a first-choice plan.

4. The “Layaway” or “Owner Financing” Long Shot

In private party sales, a motivated seller might agree to an owner-financing arrangement with a shorter term (3-5 years) and a simple contract. This bypasses bank rules. Alternatively, some specialty dealerships or clubs offer layaway plans where you make payments into an escrow account and only take possession when the total is paid. These are rare and require trust and clear contracts, but they avoid traditional long-term loan structures.

Actionable Checklist: Before You Sign on That 180-Month Dotted Line

If you’re still considering this after all warnings, run through this list. If you can’t answer “yes” to most of these, walk away.

- Is my interest rate at or below 5%? Anything higher makes the total cost obscene.

- Do I have a 20%+ down payment? This is non-negotiable for avoiding immediate negative equity.

- Do I have a stable, high-income job I expect to keep for 15 years? Job loss with this loan is a catastrophic event.

- Do I have a fully-funded emergency fund (6+ months of expenses) separate from this car?

- Do I own my home and have no other consumer debt (credit cards, personal loans)? This should be your only debt.

- Do I have a written plan to make extra principal payments monthly?

- Have I run the numbers through an auto loan calculator to see the total interest paid? (See the $24,480 example above—let that sink in).

- Have I insured the car for “gap” coverage? This is essential if you’re upside-down.

- Am I emotionally prepared to own a 15-year-old car for the next 15 years? The C6 Z06 you buy today will be a 28-year-old car when this loan ends.

The Bottom Line: The 180-Month C6 Z06 Loan is a Financial Tightrope

A C6 Z06 for sale with a 180-month finance term is not a product; it’s a financial proposition. The proposition is: “Trade $20,000+ in future interest and 15 years of being shackled to depreciating debt for a lower monthly payment today.” For 99% of people, this is a terrible trade. The Z06 is a car to be enjoyed, not a burden to be endured for 180 months.

The smart path is harder. It requires patience, saving, and a larger down payment. It means buying a slightly older C6 Z06 with higher miles to stay within a cash budget. It means financing for 60 months and paying it off early. The thrill of the LS7’s roar is real, but the freedom of owning it outright—and having your money working for you instead of against you—is a far sweeter, and more sustainable, victory. Don’t let the seductive math of a long-term loan drown out the clear, cold logic of total cost of ownership. Your future self, looking at a paid-off Corvette in the garage and a healthy bank account, will thank you for saying “no” to the 180-month trap.