Can You Have Multiple Roth IRAs? The Complete Guide To Maximizing Your Retirement Savings

Can you have multiple Roth IRAs? It’s a question that puzzles many savvy retirement savers. You’ve heard about the incredible benefits of a Roth IRA—tax-free growth, tax-free withdrawals in retirement, and no required minimum distributions (RMDs). Naturally, you might wonder if opening more than one is a smart strategy to supercharge your savings or gain access to better investment choices. The short answer is yes, you absolutely can have multiple Roth IRA accounts. The Internal Revenue Service (IRS) does not limit the number of Roth IRA accounts an individual can own. However, the real story is far more nuanced and hinges on a critical, non-negotiable rule: your total annual contributions across all your Roth IRAs cannot exceed the annual contribution limit.

This seemingly simple permission opens up a world of strategic possibilities—and potential pitfalls. Having multiple accounts can help you diversify your investment platform, utilize different financial institutions' strengths, or even facilitate complex planning like the "backdoor Roth" strategy for high earners. But it also introduces complexity in tracking contributions, managing fees, and understanding the aggregate rules that govern them. This comprehensive guide will dismantle the confusion, walking you through every rule, benefit, and consideration. We’ll explore the precise IRS regulations, dive deep into contribution limits, analyze the pros and cons of using multiple providers, and provide actionable strategies to help you decide if multiple Roth IRAs align with your unique financial blueprint.

Understanding the IRS Stance on Multiple Roth IRAs

The foundation of your entire question rests on the IRS's official position. According to IRS Publication 590-A, there is no restriction on the number of Individual Retirement Arrangements (IRAs), including Roth IRAs, that you can maintain. You can open a Roth IRA at a traditional brokerage, a robo-advisor, a bank, and a credit union simultaneously. The IRS views all of your traditional, Roth, and SEP-IRAs as a single portfolio for the purpose of aggregate contribution limits. This is the cardinal rule. You are not allowed to contribute $6,500 to a Vanguard Roth IRA and another $6,500 to a Fidelity Roth IRA in the same year. The limit applies to the sum total of your contributions across all Roth IRA accounts.

This framework is designed for flexibility, not for doubling your tax-advantaged savings room. The rationale is that the tax benefit is tied to the individual, not the account. Therefore, your ability to fund these accounts is capped annually regardless of where you hold them. This distinction is crucial. Before you rush to open a second or third account, you must internalize this: more accounts do not mean more contribution capacity. Your first step in strategizing is to calculate your maximum allowable contribution for the year, then decide how to allocate that money across your chosen platforms.

Navigating Aggregate Contribution Limits: The Non-Negotiable Rule

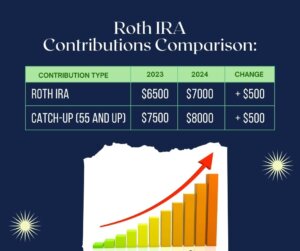

Let’s translate the IRS rule into practical, actionable numbers. For the 2024 tax year, the Roth IRA contribution limit is $7,000 if you are age 50 or older (including a $1,000 catch-up contribution), and $6,500 if you are under 50. These limits are subject to annual inflation adjustments. However, your ability to contribute to a Roth IRA at all is phased out at higher income levels.

For 2024, the phase-out range is:

- Single Filers & Heads of Household: $146,000 to $161,000

- Married Filing Jointly: $230,000 to $240,000

- Married Filing Separately: $0 to $10,000 (effectively prohibiting contributions for most)

If your Modified Adjusted Gross Income (MAGI) falls within the phase-out range, your maximum contribution is reduced proportionally. If your MAGI exceeds the top of the range, you cannot make a direct contribution to a Roth IRA for that year. This is where the strategy of multiple accounts often intersects with the "Backdoor Roth IRA" technique, which involves making a non-deductible contribution to a traditional IRA and then converting it to a Roth IRA. Having multiple traditional and Roth IRA accounts can complicate the pro-rata rule during a conversion, a topic we will cover in detail later.

Practical Example: Sarah, 35, single, has a MAGI of $150,000 in 2024. She falls within the phase-out range. Her reduced contribution limit would be calculated as follows: ($161,000 - $150,000) / ($161,000 - $146,000) = $11,000 / $15,000 = 0.733. Her maximum contribution is $6,500 * 0.733 = approximately $4,765. This $4,765 is her total contribution limit across all her Roth IRAs for the year.

Key Takeaway: Always determine your aggregate, reduced contribution limit first. Use the IRS worksheets in Publication 590-A or a reliable online calculator. Then, and only then, decide how to distribute that single lump sum across your multiple accounts.

Strategic Advantages of Using Different Providers

Now that we’ve established the hard limit, let’s explore the "why." Why would someone intentionally manage multiple Roth IRA accounts when one seems simpler? The primary driver is investment strategy and platform specialization. No single financial institution is the best at everything. Different providers excel in different areas:

- Discount Brokerages (e.g., Fidelity, Charles Schwab, Vanguard): Often have extensive commission-free ETF and mutual fund lineups, superior research tools, and low-cost index fund options. Ideal for a core, buy-and-hold portfolio.

- Robo-Advisors (e.g., Betterment, Wealthfront): Offer automated portfolio management, tax-loss harvesting, and hands-off rebalancing for a small management fee. Perfect for investors who want a set-it-and-forget-it approach.

- Specialty Platforms: Some platforms may offer unique assets like fractional shares of expensive stocks, cryptocurrency trading, or access to alternative investments (like private credit or real estate crowdfunding) within an IRA wrapper.

- Banks & Credit Unions: May offer high-yield savings or CD options within an IRA, which can be useful for the fixed-income or cash portion of your portfolio, though returns are typically lower long-term.

By holding multiple Roth IRAs, you can construct a "best-of-both-worlds" portfolio. For instance, you might keep your broad U.S. and international stock index funds at a low-cost brokerage like Vanguard, while allocating a small portion to a thematic tech ETF only available at another platform via a second Roth IRA. You could use a robo-advisor for a portion of your assets to benefit from automated tax management, while maintaining direct control over another portion. This allows for granular strategy implementation that a single provider might not fully support.

When and How to Consolidate Your Roth IRAs

The flip side of having multiple accounts is the administrative burden. Tracking contributions, managing fees, and handling paperwork for three different institutions can become a chore. This leads many to consider consolidation—rolling over multiple Roth IRAs into a single account. The process is straightforward: you request a direct trustee-to-trustee transfer from the old institution to the new one. This avoids any tax withholding and the 60-day rollover rule.

Pros of Consolidation:

- Simplified Management: One login, one statement, one set of rules to remember.

- Fee Reduction: Eliminate account maintenance fees from smaller, inactive accounts.

- Clear Performance View: See your entire Roth IRA portfolio’s performance in one place.

- Simplified RMD Planning (for beneficiaries): Easier for your heirs to manage a single inherited account.

Cons of Consolidation:

- Loss of Platform-Specific Benefits: You may give up access to unique investments or tools from the abandoned platform.

- Potential for Over-Concentration: If all your money is in one place, you are fully exposed to that institution’s operational risks (though SIPC protection applies).

- Inconvenience: You may need to sell certain holdings to transfer them, potentially triggering a taxable event if those holdings are not in-kind transfer eligible.

Actionable Tip: Before consolidating, create a spreadsheet listing all your Roth IRAs, their holdings, expense ratios, and any unique features. Identify if any holding is "unique" to its current platform. If so, you may need to sell it (potentially incurring taxes if it’s a non-qualified investment within the IRA) or leave that small account as-is.

Tax Implications and Penalties to Avoid

Multiple Roth IRAs amplify the importance of meticulous record-keeping, primarily due to the ordering rules for distributions and the risk of excess contributions.

1. The Ordering Rules: When you take a distribution, the IRS assumes the money comes out in this order: regular contributions first (always tax- and penalty-free), then conversions (on a first-in, first-out basis, each conversion batch subject to its own 5-year rule), then earnings. If you have multiple Roth IRAs, the IRS aggregates them for these rules. It doesn’t matter which account the money comes from; the IRS treats all your Roth IRAs as one. Therefore, you must track your total basis (non-deductible contributions) across all accounts using IRS Form 8606 every year you make a non-deductible contribution or a conversion. Failing to file this form can lead to double taxation.

2. Excess Contribution Penalties: If you accidentally contribute more than your aggregate limit across all accounts, you must correct it by the tax filing deadline (including extensions) to avoid a 6% excise tax per year on the excess amount. The correction involves withdrawing the excess contributions and any earnings on them before the deadline. If you miss the deadline, the excess is subject to the 6% penalty each year it remains in the IRA.

3. The Pro-Rata Rule & Conversions: This is a major pitfall when multiple IRAs exist. When you convert any amount from a traditional IRA to a Roth IRA, the IRS looks at all your traditional, SEP, and SIMPLE IRAs across all institutions as of December 31st of the conversion year. The taxable portion of your conversion is calculated pro-rata based on the total pre-tax vs. after-tax (non-deductible) basis in all these accounts. Having multiple traditional IRAs with pre-tax money can make a "backdoor Roth" conversion significantly more taxable than you expect. This rule is why many high earners with large pre-tax IRA balances find the backdoor Roth strategy inefficient.

Roth IRA Conversions: Rules and Strategies

Conversions are a powerful tool, and multiple accounts can be used strategically here. A conversion moves money from a traditional IRA (tax-deferred) to a Roth IRA (tax-free), paying ordinary income tax on the converted amount in the year of conversion.

Key Rules:

- No Income Limit: Since 2010, anyone can convert, regardless of income.

- 5-Year Rule: Each conversion batch has its own 5-year clock for penalty-free withdrawal of that converted amount (you must be 59½ or meet another exception). If you have multiple Roth IRAs from conversions, you must track each batch’s 5-year period separately.

- Tax Calculation: As mentioned, the pro-rata rule applies across all traditional IRAs. To isolate a non-deductible basis for a clean conversion, you must either:

- Roll all pre-tax traditional IRA funds into an employer-sponsored 401(k) plan (if the plan accepts roll-ins), leaving only after-tax basis in your IRAs, then convert.

- Accept that conversions from multiple IRAs will be partially taxable based on the overall ratio.

Strategic Use of Multiple Accounts: Some investors use a separate Roth IRA specifically for conversions to keep the accounting clean. They might convert a small amount each year to stay in a lower tax bracket, directing each year’s conversion into a distinct Roth IRA account to easily track its individual 5-year rule.

Income Limits and Eligibility Requirements

We’ve touched on this, but it bears its own section. Your ability to contribute directly to a Roth IRA is strictly limited by your MAGI. These limits are adjusted annually. For 2024, as noted, the phase-out for married filing jointly is $230,000 to $240,000. If your income is above these limits, a direct contribution is prohibited.

However, the "Backdoor Roth IRA" remains a viable, legal workaround for high earners. The process: 1) Contribute $6,500 (or $7,000) to a non-deductible traditional IRA. 2) Immediately convert that traditional IRA to a Roth IRA. Because you used after-tax dollars for the initial contribution, the conversion is largely tax-free (except for any minimal growth between contribution and conversion).

Why Multiple Accounts Matter Here: The pro-rata rule (see above) is the backdoor Roth’s greatest enemy. If you have any other pre-tax money in any traditional, SEP, or SIMPLE IRA across all your financial institutions, the IRS will tax a proportional share of your conversion as ordinary income. This can turn a tax-free maneuver into a taxable event. Therefore, high earners considering the backdoor Roth must either:

- Have zero pre-tax IRA balances across all institutions, or

- Be willing to pay the pro-rata tax, or

- Roll pre-tax IRA funds into an employer 401(k) first.

Spousal Roth IRAs and Family Planning

A powerful and often overlooked feature is the Spousal Roth IRA. Even if one spouse has little or no earned income, the working spouse can contribute to a Roth IRA on behalf of the non-working spouse, provided they file a joint tax return. The total contributions for both spouses cannot exceed the total earned income of the couple, and each spouse’s contribution is subject to the standard annual limit and income phase-outs based on their joint MAGI.

How Multiple Accounts Apply: A married couple can, and often should, have separate Roth IRA accounts in each spouse’s name. This is not about circumventing limits—each spouse has their own independent contribution limit—but about estate planning and beneficiary management. Having separate accounts simplifies required minimum distributions for heirs (before the SECURE Act changes) and allows for different investment strategies based on each spouse’s risk tolerance and time horizon. The working spouse’s contributions to the non-working spouse’s Roth IRA are direct contributions to that spouse’s account, not a joint account.

The End of Recharacterization (Mostly)

Prior to the Tax Cuts and Jobs Act of 2017, you could "recharacterize" (undo) a Roth IRA conversion or contribution up until the tax filing deadline (including extensions). This was a valuable safety net. If your Roth IRA investments tanked after a conversion, you could recharacterize it back to a traditional IRA, avoiding the tax bill. For conversions completed in 2018 or later, recharacterizations are no longer allowed. Once you convert, it’s permanent for tax purposes.

However, you can still recharacterize a contribution (not a conversion) that you made directly to a Roth IRA. For example, if you contributed to a Roth IRA but later realize your income was too high, you can recharacterize that contribution as a traditional IRA contribution by the deadline. This rule still applies, but it’s more limited. The inability to undo conversions makes the decision to convert—and the timing of that decision with multiple accounts—much more critical. You must be confident in your market timing and tax situation before clicking "convert."

Roth IRAs and Required Minimum Distributions (RMDs)

Here is a monumental benefit of the Roth IRA: Original owners of Roth IRAs are not subject to Required Minimum Distributions (RMDs) during their lifetime. This is true regardless of how many Roth IRAs you have. Your money can continue to grow tax-free indefinitely. This is a stark contrast to traditional IRAs and 401(k)s, which force you to take taxable distributions starting at age 73 (as of the SECURE Act 2.0).

Important Beneficiary Note: While you don’t have RMDs, your beneficiaries will. Under the SECURE Act 2.0, most non-spouse beneficiaries must withdraw and fully deplete inherited Roth IRAs within 10 years of the original owner’s death. Having multiple Roth IRAs does not change this 10-year rule, but it can complicate the administration for the beneficiary, who must manage the RMDs (or full distribution) across multiple accounts. This is a strong argument for consolidating Roth IRAs later in life to simplify your estate.

Beneficiary Rules and Estate Planning Considerations

Designating beneficiaries for your Roth IRAs is a crucial part of your estate plan. You can name primary and contingent beneficiaries directly on each IRA account. Because Roth IRAs are funded with after-tax dollars, they are incredibly valuable to heirs, who can then withdraw the money tax-free (provided the account has been open for at least 5 years).

Strategies with Multiple Accounts:

- Tiered Beneficiary Designations: You could use different Roth IRAs to leave assets to different beneficiaries (e.g., one for a child, one for a grandchild) with tailored investment strategies.

- Trusts as Beneficiaries: You can name a trust as a beneficiary, but complex rules (the "see-through trust" requirements) apply. Having multiple accounts might mean multiple trust documents, adding complexity.

- Charitable Remainder Trusts (CRTs): A Roth IRA can be used to fund a CRT, providing an income stream to a beneficiary with the remainder going to charity. This is an advanced strategy where having a dedicated Roth IRA for this purpose can be useful.

The overarching advice is to keep your beneficiary designations up-to-date on every Roth IRA account you own after major life events (marriage, divorce, birth of a child). Inconsistencies or outdated designations can lead to assets going to unintended parties.

When to Seek Professional Financial Advice

Given the intricate interplay of contribution limits, income phase-outs, the pro-rata rule, and estate planning, multiple Roth IRAs are a situation where professional advice often pays for itself. You should strongly consider consulting a fee-only financial planner or a CPA if:

- Your income is near or above the Roth IRA phase-out range and you are considering the backdoor Roth strategy.

- You have significant pre-tax balances in traditional, SEP, or SIMPLE IRAs and are contemplating conversions.

- You are approaching retirement and are strategizing Roth conversions to manage future tax brackets.

- Your estate is complex, involving multiple beneficiaries, trusts, or charitable goals.

- You simply feel overwhelmed by the bookkeeping and want a consolidated strategy.

A professional can run the numbers, model different scenarios (e.g., converting $X in year Y vs. Z), and ensure your multiple accounts are working in concert toward your goals, not against you with hidden tax traps.

Conclusion: Yes, But With a Strategic Plan

So, can you have multiple Roth IRAs? Absolutely. The IRS grants you the freedom to open as many as you desire. But with that freedom comes the immutable responsibility of the aggregate contribution limit. The decision to utilize multiple accounts should be a deliberate strategy, not a casual convenience. For the disciplined investor, multiple Roth IRAs can be a powerful toolkit: enabling platform specialization, facilitating sophisticated conversion strategies, and allowing for nuanced beneficiary planning. For the disorganized, they are a recipe for costly errors—excess contributions, mis-tracked basis, and inefficient conversions.

Before you open that second or third account, ask yourself: What specific strategic advantage does this new platform provide that my current one does not? Can I achieve the same goal by simply buying a different ETF in my existing account? Will the administrative complexity outweigh the potential benefit? And most importantly, have I calculated my exact, reduced contribution limit for the year and ensured my total contributions across all accounts stay within it?

Ultimately, the goal is the same: to build a large pool of tax-free money for your retirement. Whether you use one Roth IRA or five, the contribution limit is your primary constraint. Focus on maxing out that limit with a sound, low-cost investment strategy in a way you can sustainably manage. If the advantages of multiple platforms are compelling for your situation, embrace them, but implement them with a meticulous tracking system and a clear understanding of the rules that bind them all together. When in doubt, the cost of a single consultation with a qualified advisor is infinitesimally smaller than the cost of a permanent tax mistake.