Can You Get FAFSA For Grad School? A Complete Guide To Graduate Financial Aid

Yes, you absolutely can get FAFSA for grad school. In fact, filling out the Free Application for Federal Student Aid (FAFSA) is the critical first step for most graduate students seeking financial assistance. The process is similar to undergraduate FAFSA completion but comes with its own set of rules, considerations, and potential aid sources. If you're asking, "can you get FAFSA for grad school?" the answer is a resounding yes, but understanding how and what you qualify for is essential to maximizing your funding package and minimizing future debt. This comprehensive guide will walk you through every detail, from eligibility to submission, ensuring you navigate the graduate financial aid landscape with confidence.

Understanding the Basics: FAFSA and Graduate School

Many prospective graduate students operate under a common misconception: that financial aid is primarily for undergraduates. This belief can derail educational plans before they even begin. The reality is that federal financial aid is available for graduate and professional students, though the types and amounts often differ significantly from what undergraduates receive. The FAFSA serves as the gateway to this aid, acting as the universal application for federal grants, work-study, and loans. It's also frequently used by states and individual colleges to determine eligibility for their own institutional grants and scholarships.

The core principle remains the same: the FAFSA calculates your Expected Family Contribution (EFC), now referred to as the Student Aid Index (SAI). This index, derived from your (and potentially your spouse's or parents') financial information, estimates your ability to pay for education. Your school then subtracts your SAI from its total cost of attendance (COA) to determine your financial need. For graduate students, the calculation of need and the types of aid that fill that need follow a specific pattern that you must understand to plan effectively.

The Key Difference: Dependency Status for Grad Students

One of the most significant shifts from undergraduate to graduate status is the dependency determination. For FAFSA purposes, you are automatically considered an independent student if you are pursuing a graduate or professional degree. This is a crucial advantage. It means you do not need to provide parental information on the FAFSA form. Your financial aid eligibility will be based solely on your (and your spouse's, if married) income, assets, and tax information. This simplifies the process immensely for students who may not have a close financial relationship with their parents or whose parents are unable or unwilling to contribute.

However, there is an important exception. While the FAFSA itself does not require parental info for grad students, some graduate schools and private scholarship providers may still request it for their own institutional aid formulas. They might use a "professional judgment" to request a FAFSA parental information form if they believe parental resources could contribute. Be prepared for this possibility, especially if you're applying for highly competitive institutional grants or fellowships. Always check your specific school's financial aid policies.

Step-by-Step: How to Complete the FAFSA for Graduate School

The mechanics of filling out the FAFSA are identical regardless of your degree level, but the context and implications are different for a grad student. Here is a structured approach to ensure accuracy and timeliness.

1. Gather Your Documents Early

Before you log in to the FAFSA on the Web (studentaid.gov), collect all necessary documentation. For graduate students, this typically includes:

- Your Social Security Number (and your spouse's, if married).

- Your driver's license (if applicable).

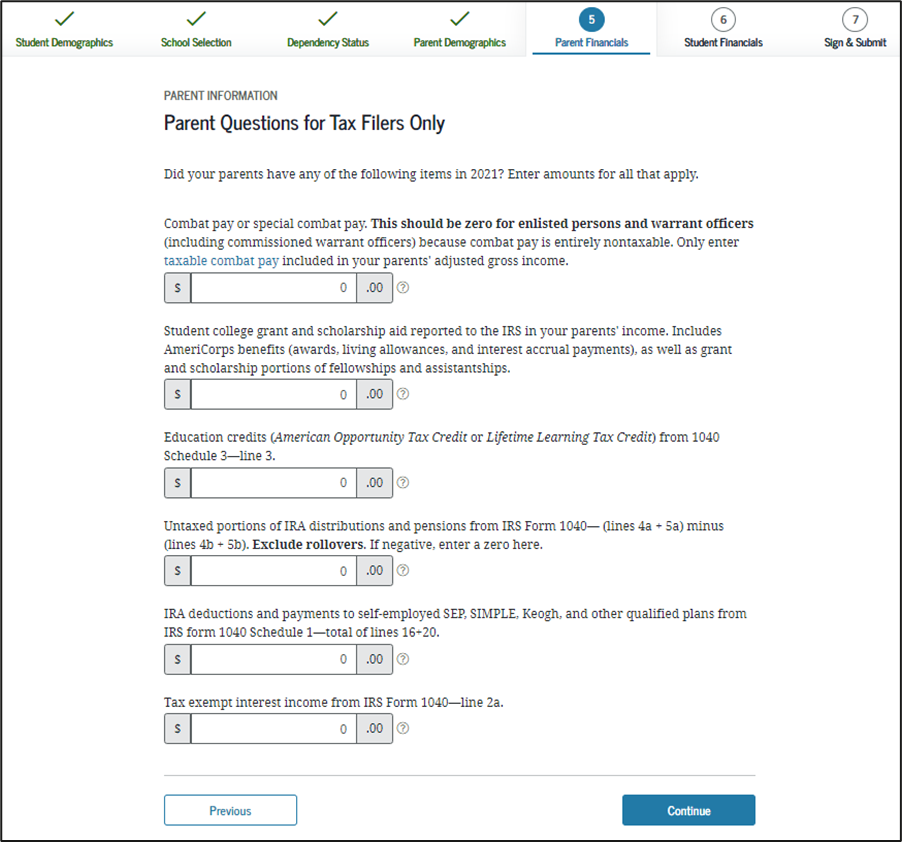

- Your most recent federal income tax return (and your spouse's, if married). For the 2024-2025 award year, you'll use your 2022 tax information. The IRS Data Retrieval Tool (DRT) can import this directly, which is highly recommended to avoid errors.

- Records of untaxed income, such as child support received, veterans benefits, or disability payments.

- Current bank statements and investment records (for you and your spouse, if applicable).

- Your school's Federal School Code. You can find this on your school's financial aid website or by using the search tool on the FAFSA site. You can list up to 10 schools to receive your information.

2. Understand the FAFSA Timeline for Grad School

The FAFSA opens on October 1st each year for the following academic year. For example, the FAFSA for the 2025-2026 school year opens on October 1, 2024. Priority deadlines are critical and vary significantly by school and state. Some graduate programs have rolling admissions or later deadlines, but financial aid funds, especially for work-study and some institutional grants, are often awarded on a first-come, first-served basis. Submit your FAFSA as close to October 1 as possible to maximize your opportunities. Mark these key dates on your calendar immediately.

3. Fill It Out Accurately and Completely

As an independent student, you will answer "No" to all dependency questions. You will report your own (and spouse's) financial information. Pay meticulous attention to:

- Correct tax year: Use the tax year specified for the award year you're applying for.

- Household size: Include yourself, your spouse (if married), and any dependents for whom you provide more than half of their support.

- Asset reporting: Report the net value of your investments and business assets accurately. This includes things like a 401(k) only if it is for a business you own. Personal retirement accounts like a traditional or Roth IRA are not reported as assets on the FAFSA, which is a key benefit for students who have saved.

4. Review, Sign, and Submit Electronically

After completing the form, review every entry. The most common FAFSA errors are simple typos in Social Security Numbers or mismatched names. You and your spouse (if applicable) must sign electronically using your FSA IDs. If you don't have an FSA ID, create one before you start the FAFSA—it can take a few days to verify your identity. Once submitted, you'll receive a Student Aid Report (SAR) within 3-5 days (if filed electronically). Review this for any errors or corrections requested by the Department of Education.

What Types of Federal Aid Can You Get for Grad School?

This is the heart of the matter. The FAFSA qualifies you for a suite of federal aid programs, but the availability and amounts for graduate students differ from undergraduates.

Federal Direct Unsubsidized Loans

This is the workhorse of graduate student aid. It is available to all eligible graduate students regardless of financial need. For the 2024-2025 academic year, the annual loan limit is $20,500. There is also an aggregate (total) lifetime limit of $138,500 for graduate students, which includes any federal subsidized or unsubsidized loans received as an undergraduate. The interest rate is set annually by Congress and is typically higher than undergraduate rates. Interest accrues while you are in school, during your grace period, and during any deferment or forbearance periods.

Federal Direct PLUS Loans for Graduate/Professional Students (Grad PLUS)

This is a credit-based federal loan designed to cover any remaining cost of attendance after other aid has been applied. You can borrow up to your school's certified COA minus any other financial aid received. The key feature is that a credit check is required. A poor credit history (e.g., recent bankruptcy, default, or delinquency) could result in denial. However, you may still be eligible if you have an endorser/co-signer (called an endorser on the PLUS loan) who does not have an adverse credit history, or if you can document extenuating circumstances related to your credit issues. The interest rate is higher than the Unsubsidized Direct Loan, and an origination fee is deducted from each disbursement.

Federal Work-Study (FWS)

This program provides part-time employment to help earn money for educational expenses. It is need-based, so your eligibility is determined by your FAFSA results. Funding is limited and awarded by your school. Not all graduate students receive FWS, and the amount can vary widely. Jobs are often on-campus or with approved off-campus employers related to your field of study, providing both income and valuable experience.

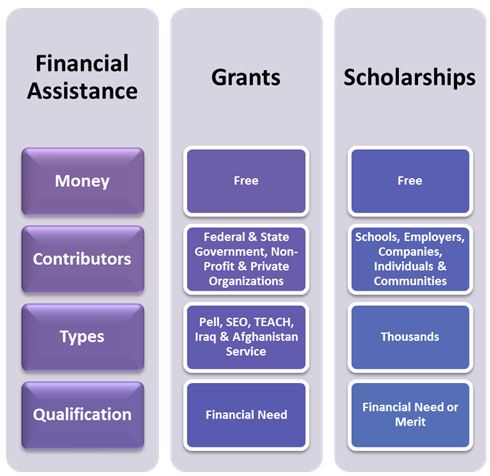

Federal Grants (Limited for Graduate Students)

This is a major point of clarification. There are almost no federal grant programs specifically for graduate students. The two primary federal grants are:

- Pell Grant: Almost exclusively for undergraduate students who have not yet earned a bachelor's or professional degree. Graduate students are ineligible.

- Federal Supplemental Educational Opportunity Grant (FSEOG): For undergraduates with exceptional financial need. Graduate students are ineligible.

The only significant federal grant potentially available to graduate students is the Teacher Education Assistance for College and Higher Education (TEACH) Grant, which requires you to be enrolled in a qualifying teaching program and commit to four years of teaching in a high-need field after graduation. If you fail to complete the service obligation, the grant converts to a Direct Unsubsidized Loan.

Institutional and State Aid: The Hidden Gems

While federal aid forms the foundation, a significant portion of graduate funding comes from your specific institution and your state of residence. This is where the FAFSA's role expands beyond just federal loans.

- Institutional Grants & Scholarships: Many graduate schools and departments offer their own need-based grants and merit-based scholarships. They almost always require the FAFSA (and sometimes a separate application) to determine eligibility for need-based awards. A strong academic profile combined with demonstrated financial need can unlock substantial funding from your university.

- State Grants: Some states offer grant programs for graduate students, particularly in high-demand fields like teaching, nursing, or STEM. For example, states like Texas, New York, and California have various programs. Residency is key—you typically must be a resident of the state to qualify. Check your state's higher education agency website for specific programs.

- Assistantships & Fellowships: While not directly awarded via the FAFSA, many graduate assistantships (research or teaching) provide a tuition waiver and a stipend. Some fellowship programs require you to file the FAFSA to be considered for the need-based components of their awards. Always ask your department about all forms of aid.

Common Mistakes and Pitfalls to Avoid

Navigating the FAFSA for grad school is straightforward, but errors can cost you thousands. Here are the most frequent missteps:

- Missing the Deadline: This is the single biggest mistake. Your school's deadline is not a suggestion; it's the cutoff for being considered for any institutional aid. Set multiple reminders.

- Not Filing at All: Assuming you won't qualify is a costly error. You won't know what you're eligible for until you apply. The FAFSA is free and takes about an hour.

- Incorrect Dependency Status: Remember, as a grad student, you are independent. Do not mistakenly include parental information unless your school specifically requests it via a professional judgment review.

- Using the Wrong Tax Year: Double-check the award year's required tax information. Using the wrong year will cause processing delays.

- Leaving Fields Blank: If a question doesn't apply, enter "0" or "N/A." Blank fields can cause your application to be rejected.

- Not Using the IRS DRT: Manually typing tax numbers is error-prone. The IRS Data Retrieval Tool is the most accurate way to transfer your tax data.

- Forgetting to Sign: An unsigned FAFSA is incomplete and unprocessable. Ensure you and your spouse (if applicable) sign electronically with your FSA IDs.

- Not Updating Your FAFSA: If your financial situation changes dramatically (e.g., loss of job, significant medical bills), contact your school's financial aid office to request a professional judgment review. They can adjust your aid package based on your new circumstances.

Actionable Tips for Maximizing Your Graduate Aid

- File Early, File Every Year: Submit your FAFSA on October 1st. You must reapply annually, so set a recurring calendar event.

- Communicate with Your Financial Aid Office: They are your best resource. Ask specific questions: "What is my priority deadline?" "Do you require parental information for institutional aid?" "What is the average debt load for students in my program?"

- Research All Funding Sources: Don't rely solely on the FAFSA. Aggressively search for:

- Departmental fellowships and assistantships.

- External scholarships from professional associations, foundations, and community organizations related to your field.

- Employer tuition reimbursement programs if you are working while studying.

- Borrow Strategically: If you need loans, exhaust Federal Direct Unsubsidized Loans first (lower interest rate, no credit check) before considering Grad PLUS Loans. Only borrow what you absolutely need after accounting for scholarships, grants, and income.

- Understand Your Cost of Attendance (COA): Your school provides an estimated COA, which includes tuition, fees, room, board, books, supplies, transportation, and personal expenses. Use this figure as your budgeting guide. Your total financial aid (all sources) cannot exceed your COA.

Addressing the Big Questions

Q: Does my parents' income affect my FAFSA for grad school?

A: No, for the federal FAFSA, it does not. As an independent student, only your (and spouse's) income and assets are used. However, as noted, some private scholarships or institutional aid may request parental information.

Q: Can I get a Pell Grant for graduate school?

A: Almost never. The Pell Grant is for undergraduate students who have not yet earned a bachelor's degree. The rare exception is if you are enrolled in a post-baccalaureate teacher certification program.

Q: What is the maximum amount of federal student loans I can get for grad school?

A: The annual limit for Federal Direct Unsubsidized Loans is $20,500. You can borrow additional amounts up to your COA via the Grad PLUS Loan, subject to a credit check. The aggregate (total) limit for all federal student loans (undergraduate + graduate) is $138,500.

Q: How does FAFSA affect my eligibility for private student loans?

A: Most private lenders do not require the FAFSA. However, having a completed FAFSA on file and exhausting all federal loan options first is a best practice. Federal loans have benefits (like income-driven repayment plans and potential forgiveness) that private loans do not.

Conclusion: Your Path to Affordable Graduate Education

So, can you get FAFSA for grad school? Absolutely. The FAFSA is not just a form; it's your primary tool for unlocking the financial resources that can make your graduate or professional degree achievable. The process empowers you as an independent student, placing the focus on your own financial situation. By understanding the nuances—from the independence status and the predominance of loans over grants to the critical importance of deadlines and school-specific policies—you transform anxiety into action.

The journey begins with a single step: completing the FAFSA on or after October 1st. Combine this with diligent research into your school's specific aid offerings, proactive communication with financial aid administrators, and a parallel hunt for external scholarships and assistantships. Remember, the most successful graduate students are often those who master the financial aid landscape just as thoroughly as their academic subject. Don't leave money on the table. File your FAFSA, explore every option, and invest in your future with a clear, informed financial plan. Your advanced degree is within reach, and understanding FAFSA for grad school is the key that opens the door.