How Soon Can I Do A HELOC After Purchasing A Home? The Ultimate Guide

Are you wondering how soon can I do a HELOC after purchasing home and unlock the equity you just built?

Buying a new house is an exciting milestone, but it also raises a practical question: when can you tap into that newly acquired equity? Many homeowners assume they must wait years before a lender will approve a home equity line of credit (HELOC). In reality, the answer depends on a mix of lender policies, your financial profile, and the timing of your closing. This guide breaks down the key factors that determine how soon can i do a heloc after purchasing home and gives you actionable steps to plan your move.

1. Eligibility Requirements for a HELOC Immediately After Closing

Most lenders look for a minimum equity threshold before they will consider a HELOC application. Even if you just closed on a property, you may already have built some equity through the down payment, closing costs, or modest market appreciation.

- Equity calculation: Equity equals the current market value of the home minus any outstanding mortgage balances.

- Typical minimum: Many banks require at least 15‑20 % equity, which often translates to a loan‑to‑value (LTV) ratio of 80‑85 % or lower.

- Credit score impact: A score of 680 or higher is generally the baseline for favorable rates, though some lenders will consider scores as low as 620 if other factors are strong.

Why it matters: Lenders want to ensure that the borrower has a cushion against market fluctuations. If you have already crossed the equity threshold, you can submit an application as early as 30‑45 days post‑closing, provided the rest of your profile meets the lender’s standards.

2. Typical Waiting Periods Set by Lenders

While some financial institutions will review a HELOC request almost immediately, others enforce mandatory waiting periods. These can range from 90 days to six months depending on the lender’s risk models.

- Bank policies: Large national banks often impose a 90‑day “seasoning” period to verify that the mortgage is performing without delinquencies.

- Credit unions: Many credit unions are more flexible and may allow applications after 30 days if the borrower has a solid payment history.

- Online lenders: Some fintech options can process a HELOC in as little as two weeks, but they may still require a short waiting period to confirm that the loan is not a “cash‑out” refinance.

Action tip: Contact multiple lenders early in your home‑buying process to compare their seasoning requirements. This comparison can shave weeks off your timeline and help you choose the most accommodating option.

3. How Your Credit Score Impacts Early HELOC Access

Your credit score is a critical determinant of both approval odds and interest rates. Even a modest dip in score can trigger stricter underwriting or higher rates.

- Score above 740: Qualifies for the best rates and may bypass additional documentation.

- Score 700‑739: Still eligible, but lenders may request additional proof of income or lower debt‑to‑income (DTI) ratios.

- Score below 700: May require a larger equity stake or a higher interest rate to offset perceived risk.

Real‑world example: Jane closed on her home in March and had a credit score of 750. She submitted a HELOC application in early May and was approved with a 4.75 % variable rate. Her neighbor, Mark, with a score of 680, had to wait until August before a lender would consider his request, and his rate was 6.25 %.

4. Loan‑to‑Value (LTV) Ratios and Early Applications

LTV is the ratio of your total mortgage debt to the home’s appraised value. It directly influences how much you can borrow and the interest rate you receive.

- Standard LTV limit: Most lenders cap HELOC LTV at 85 % of the home’s value.

- Combined LTV (CLTV): When you factor in your primary mortgage, the combined debt (first mortgage + HELOC) often cannot exceed 90‑95 % of the home’s value.

- Early equity boost: If your home’s appraisal comes in higher than expected, you may achieve a lower CLTV, making early approval more likely.

Key takeaway: Even if you have only a small amount of equity, a high appraisal can improve your LTV, allowing you to qualify for a HELOC sooner.

5. Documentation You’ll Need to Provide

Lenders require a consistent set of documents to verify income, assets, and the property’s value. The sooner you gather these, the faster the approval process.

- Proof of income: Recent pay stubs, tax returns, and W‑2 forms.

- Asset statements: Bank statements showing sufficient reserves for closing costs and closing cash.

- Property information: The settlement statement (HUD‑1), deed, and any appraisal reports.

- Credit verification: A recent credit report or a credit monitoring service snapshot.

Bullet list of essentials:

- Recent pay stubs (last 30 days)

- Two years of tax returns

- Bank statements (last 2 months)

- Mortgage payoff statement (if applicable)

- Home appraisal (if already ordered)

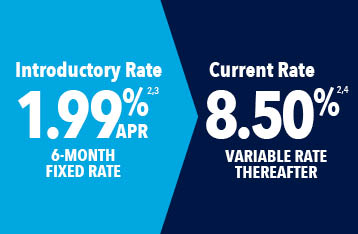

6. Interest Rate Considerations for New Homeowners

Interest rates on HELOCs can be variable or fixed, and they are influenced by broader market conditions as well as your personal risk profile.

- Variable rates: Typically tied to the prime rate; they can fluctuate monthly, affecting your payment amount.

- Fixed‑rate options: Some lenders offer a “fixed‑rate conversion” after a certain period, giving you payment certainty.

- Rate discounts: A strong credit score, low LTV, or existing relationship with the bank can earn you a rate reduction of 0.25‑0.5 %.

Actionable tip: If you anticipate needing funds for home improvements or debt consolidation, locking in a fixed rate early can protect you from rising market rates. However, be aware that fixed‑rate HELOCs often come with higher initial rates than their variable counterparts.

7. Alternative Financing Options If You’re Not Ready

If the waiting period or lender requirements feel restrictive, there are alternatives to consider before committing to a HELOC.

- Cash‑out refinance: Allows you to refinance your primary mortgage for more than the existing balance, pulling out equity in one lump sum.

- Home equity loan: Similar to a HELOC but structured as a second‑mortgage with a fixed payment schedule.

- Personal loan: Unsecured loans can be used for smaller projects and may have quicker approval timelines.

- Savings or investment withdrawal: If you have a disciplined savings plan, tapping those funds avoids borrowing altogether.

When to choose each:

- Cash‑out refinance – Best when you need a large amount and want a single, predictable payment.

- Home equity loan – Ideal for one‑time expenses like major renovations.

- Personal loan – Suitable for modest, short‑term financing needs.

8. Real‑World Examples: When Did Homeowners Successfully Secure a HELOC?

Examining case studies helps illustrate how soon can i do a heloc after purchasing home in practice.

- Case A – Aggressive Lender: A homeowner in Austin closed on a $350,000 property in January. With a 20 % down payment and a 780 credit score, they applied for a HELOC in early February and received approval by the end of the month, accessing $30,000 at a 4.5 % variable rate.

- Case B – Conservative Approach: In Detroit, a buyer purchased a $250,000 home in June with a 10 % down payment. Their credit score was 710, and the lender required a 90‑day seasoning period. They were approved in late September, after building $15,000 in equity through market appreciation.

- Case C – Low‑Equity Scenario: A buyer in Phoenix made a 5 % down payment on a $400,000 home. Because their LTV was 95 %, they could not qualify for a HELOC until they paid down the mortgage enough to bring the LTV below 85 %, which occurred after 10 months of regular payments.

These examples underscore that timing, equity, credit, and lender choice all intersect to determine the earliest possible HELOC access.

Conclusion

Understanding how soon can i do a heloc after purchasing home hinges on a blend of equity, creditworthiness, lender policies, and timing. While some borrowers can secure a HELOC within a month of closing, others may need to wait several months to meet seasoning or LTV thresholds. By proactively gathering documentation, shopping around for flexible lenders, and monitoring your credit score, you can position yourself to tap into your home’s equity as soon as the financial math works in your favor. Whether you’re planning renovations, consolidating debt, or building a financial safety net, knowing the timeline empowers you to make confident, well‑timed decisions about your home’s future.