How Many Roth IRAs Can You Have? The Surprising Answer

Wondering how many Roth IRAs you can have? You're not alone. This common question often stems from a desire to maximize retirement savings, organize funds separately for different goals, or take advantage of specific investment options at various institutions. The short answer might surprise you: There is no legal limit on the number of Roth IRA accounts you can own. You could theoretically open one at every brokerage, bank, and mutual fund company in the country. However, the real constraint isn't the number of accounts—it's the annual contribution limit that applies across all your Roth (and traditional) IRAs combined. This crucial distinction between account quantity and contribution capacity is the cornerstone of understanding Roth IRA rules and optimizing your retirement strategy.

This guide will dismantle the myth of a "Roth IRA count limit" and replace it with a clear, actionable framework. We'll navigate the annual contribution caps, income-based eligibility rules, the powerful "backdoor Roth" strategy, and the nuanced situations involving spousal accounts, conversions, and inherited IRAs. By the end, you'll know exactly how to structure your Roth IRA holdings for maximum tax-free growth and flexibility, all while staying firmly within IRS regulations. Let's turn that initial question into a comprehensive retirement plan.

The Core Rule: Unlimited Accounts, But One Annual Contribution Bucket

No Legal Cap on the Number of Roth IRA Accounts

The Internal Revenue Service (IRS) does not impose a limit on how many individual Roth IRA accounts you can establish. You are free to open a Roth IRA at Fidelity, another at Vanguard, a third at a local credit union, and so on. This flexibility is a powerful tool for investors. You can use multiple Roth IRAs to segregate investments, such as holding aggressive growth funds in one account and more conservative bonds in another, simplifying portfolio management. It also allows you to access different platforms' unique offerings, like specific ETFs, commission-free trades, or proprietary research tools. Furthermore, spreading assets across multiple financial institutions can be a component of a broader asset protection or diversification strategy.

However, this freedom comes with a critical administrative responsibility. You are solely responsible for tracking your total contributions across all your Roth and traditional IRAs to avoid exceeding the annual limit. The custodian (the bank or brokerage where you open an account) reports contributions to the IRS, but they only see the activity in their specific account. The IRS aggregates the data from all institutions. An "excess contribution" is one of the most common and costly IRA mistakes, triggering a 6% excise tax each year the error remains uncorrected. Therefore, while you can have many accounts, you must maintain meticulous records or use consolidated tracking software to ensure compliance.

The Single Annual Contribution Limit Applies Across All IRAs

This is the non-negotiable rule that governs your ability to fund your Roth IRAs. For the 2024 tax year, the maximum total contribution you can make to all of your Roth and traditional IRAs combined is $7,000. If you are age 50 or older, you can contribute an additional $1,000 as a "catch-up" contribution, bringing your total to $8,000. This limit is per person, not per account.

Let's illustrate with a practical example:

- Kellyanne Conway Fred Thompson

- Carlyjane Onlyfan Leak

- Kannadamovierulzcom Download 2024

- Christopher Papakaliatis

- Scenario A: You have one Roth IRA at Brokerage X. You contribute the full $7,000 to it. You have now used your entire annual contribution capacity. You cannot contribute any more money to a Roth or traditional IRA at any other institution for that tax year.

- Scenario B: You have two Roth IRAs—one at Brokerage Y and one at Brokerage Z. You contribute $4,000 to the account at Y and $3,000 to the account at Z. Your total contribution is $7,000, which is exactly the limit. You are compliant.

- Scenario C (The Mistake): You have three Roth IRAs. You contribute $5,000 to Account 1, $5,000 to Account 2, and $2,000 to Account 3. Your total is $12,000. You have exceeded the $7,000 limit by $5,000. That $5,000 is an excess contribution. You must withdraw it (and any earnings on it) by the tax filing deadline, including extensions, to avoid the 6% penalty.

Key Takeaway: Think of your annual IRA contribution limit as a single bucket of money. You can pour that water into one big bucket (one IRA) or split it among several smaller buckets (multiple IRAs), but the total amount of water cannot exceed the bucket's capacity.

Eligibility: The Income Limits That Truly Matter

The Roth IRA Income Phase-Out Ranges

Having multiple accounts doesn't change your fundamental eligibility to contribute to a Roth IRA. That eligibility is determined by your Modified Adjusted Gross Income (MAGI) and your filing status. For 2024, if your MAGI falls below a certain threshold, you can contribute the full amount. As your income rises, your allowable contribution is gradually reduced ("phased out") until it reaches zero at the upper end of the range.

The 2024 phase-out ranges are:

- Single Filers & Head of Household: $146,000 to $161,000

- Married Filing Jointly: $230,000 to $240,000

- Married Filing Separately: $0 to $10,000 (if you lived with your spouse at any time during the year)

If your income is above the top of these ranges, you cannot make a direct contribution to a Roth IRA for that tax year. However, this is where the strategy of multiple accounts and the "backdoor Roth" comes into play, which we will explore in detail later.

How to Calculate Your Reduced Contribution

If your MAGI is within the phase-out range, you must calculate your reduced contribution limit. Here’s the formula:

- Determine your MAGI.

- Subtract the lower end of the phase-out range for your filing status from your MAGI.

- Divide that result by $15,000 (for single/head of household) or $10,000 (for married filing jointly).

- Multiply the result by the maximum contribution limit ($7,000 or $8,000).

- Subtract that number from the maximum contribution limit to find your reduced amount.

Example (2024, Single Filer): Your MAGI is $155,000.

- $155,000 - $146,000 = $9,000

- $9,000 / $15,000 = 0.6

- 0.6 * $7,000 = $4,200

- $7,000 - $4,200 = $2,800 (your reduced contribution limit)

You could put this $2,800 into one Roth IRA or split it among several. The math is the same.

Strategic Reasons to Use Multiple Roth IRA Accounts

Investment Platform Specialization and Cost Optimization

Different investment platforms have different strengths. One might offer a vast array of commission-free ETFs with low expense ratios, another might have superior options for trading individual stocks or accessing certain mutual funds, and a third might provide exceptional banking integration or automated investing tools. By holding multiple Roth IRAs, you can "shop the marketplace" for the best vehicle for each portion of your portfolio. For instance, you might use Brokerage A for your core S&P 500 index fund, Brokerage B for a specialized sector ETF not available elsewhere, and Brokerage C for a certificate of deposit (CD) ladder within your Roth for stability. This allows you to minimize costs and maximize access without being locked into a single provider's sometimes-limited menu.

Streamlining for Specific Financial Goals

A powerful psychological and organizational benefit of multiple Roth IRAs is goal-based account labeling. You can open separate Roth IRAs and name them for distinct objectives:

- "Roth IRA - Tech Growth" for aggressive, long-term investments.

- "Roth IRA - Dividend Income" for a portfolio focused on generating future taxable income (though Roth withdrawals are tax-free, the dividends can be reinvested).

- "Roth IRA - Emergency Fund Backup" (remember, Roth IRA contributions can be withdrawn penalty-free anytime, making them a potential last-resort emergency fund).

This clarity helps you stay disciplined, track progress toward different milestones (like a first home down payment vs. retirement), and prevent you from taking undue risks with money earmarked for a nearer-term goal.

Facilitating Complex Strategies: The Backdoor Roth IRA

For high earners disqualified from direct Roth contributions by the income limits, the "Backdoor Roth IRA" is a critical workaround. This multi-step process involves:

- Making a non-deductible (after-tax) contribution to a Traditional IRA.

- Converting that Traditional IRA balance to a Roth IRA shortly thereafter.

This is where having multiple accounts becomes strategically useful, though not strictly necessary. Many financial advisors recommend executing the backdoor Roth using two separate IRAs at the same institution to simplify paperwork and tracking. You open a Traditional IRA (Account A), fund it with the non-deductible contribution, and then immediately convert that money into a newly opened Roth IRA (Account B). Keeping them separate creates a clean paper trail for the IRS, clearly showing the non-deductible contribution and the subsequent conversion. While you can do it with one Traditional IRA that you later convert, using two accounts reduces confusion and the risk of commingling pre-tax and after-tax dollars, which would trigger complex pro-rata rule calculations and potential tax liabilities.

Conversions, Inherited Accounts, and Spousal Rules

Roth IRA Conversions: Adding Complexity, Not Limits

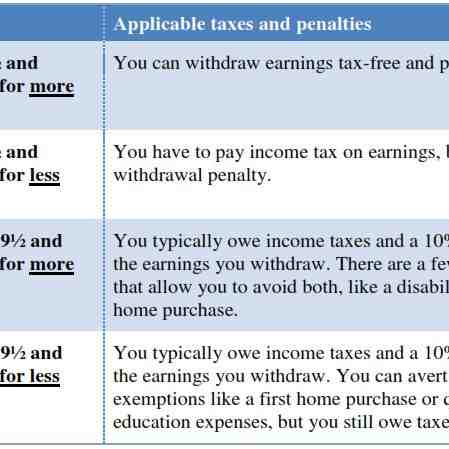

A Roth IRA conversion is the process of moving money from a tax-deferred Traditional IRA (or other eligible retirement plan) into a Roth IRA, paying ordinary income tax on the converted amount in the year of conversion. You can have as many Roth IRAs as you want to receive these conversions. There is no limit on the dollar amount you can convert in a given year. However, converting a large sum can push you into a higher tax bracket, so strategic partial conversions over several years are common.

Crucially, converted funds are subject to a 5-year holding period rule before they can be withdrawn penalty-free (the rule applies separately to each conversion). Having multiple Roth IRAs does not change this rule; the 5-year clock starts for each conversion amount in the year it occurs, regardless of which Roth account receives it. This makes tracking conversions across multiple accounts even more important.

Inherited Roth IRAs: A Separate Universe

If you inherit a Roth IRA from a deceased original owner, you establish an Inherited Roth IRA (sometimes called a Beneficiary Roth IRA). This is a distinct type of account with its own rules, most notably the 10-year distribution rule for most non-eligible designated beneficiaries (those who are not the spouse, minor child, disabled, chronically ill, or not more than 10 years younger than the deceased). You can have an Inherited Roth IRA from one parent and another from a different relative. These inherited accounts do not count against your own annual contribution limits because you cannot contribute new money to an inherited IRA. They are purely distribution vehicles. You may choose to transfer an inherited Roth IRA to a different custodian for better investment options or lower fees, effectively creating a new inherited account at a new institution, but the underlying asset and required minimum distributions (RMDs—though Roth IRAs generally have no RMDs for original owners, inherited ones do under the 10-year rule) remain governed by the decedent's account.

Spousal Roth IRAs: Funding a Partner's Future

A married couple can each have their own Roth IRA, even if one spouse has little or no earned income. This is the spousal IRA rule. The working spouse can contribute to an IRA (Roth or traditional) in the name of the non-working spouse, provided the total contributions for both spouses do not exceed their combined earned income. For example, if you earn $100,000 and your spouse earns $0, you can contribute $7,000 to your own Roth IRA and $7,000 to a separate Roth IRA in your spouse's name, for a total of $14,000, as long as your earned income ($100,000) exceeds the total contribution ($14,000). Each spouse's Roth IRA is their own individual account. You could each have multiple Roth IRAs, but the combined contribution for each person is still subject to the individual annual limit and their respective income phase-outs (which are based on the couple's joint MAGI for married filing jointly).

The Backdoor Roth IRA: A High-Income Earner's Essential Tool (Expanded)

Step-by-Step Execution and the Pro-Rata Rule Warning

For 2024, the ability to make a direct Roth IRA contribution phases out completely for singles with MAGI over $161,000 and married couples filing jointly with MAGI over $240,000. The backdoor Roth is their primary path to Roth IRA benefits. The classic, cleanest method is:

- Contribute: Fund a new Traditional IRA with a non-deductible, after-tax contribution of up to $7,000 ($8,000 if 50+). This contribution is not tax-deductible.

- Convert: Immediately convert that entire Traditional IRA balance to a new Roth IRA. Since the contribution was after-tax, the conversion should be largely tax-free. Any minimal earnings between contribution and conversion are taxable.

The Pro-Rata Rule Trap: The IRS looks at all your Traditional, SEP, and SIMPLE IRAs across all institutions when calculating the taxable portion of a conversion. If you have pre-tax money in any of these accounts, the IRS will treat your conversion as coming proportionally from both after-tax and pre-tax dollars. This can create an unexpected tax bill.

- Clean Backdoor: You have $0 in all other pre-tax IRAs. You contribute $6,000 after-tax to a new Traditional IRA and convert it to a Roth. Taxable amount = $0 (ignoring negligible earnings).

- Messy Backdoor: You have a $94,000 pre-tax balance in an old 401(k) that you rolled into a Traditional IRA at Brokerage X. You then contribute $6,000 after-tax to a new Traditional IRA at Brokerage Y and convert it. The IRS sees your total IRA balance as $100,000 ($94k pre-tax + $6k after-tax). Your conversion is deemed to be 6% ($6k/$100k) after-tax and 94% pre-tax. You would owe income tax on 94% of the converted $6,000 ($5,640), defeating the purpose.

Solution: To execute a clean backdoor Roth, you generally need to have no pre-tax IRA balances. This often requires rolling those pre-tax IRA funds into an employer's 401(k) plan first. Using separate IRAs at the same institution for the contribution and conversion (as mentioned earlier) is an administrative best practice but does not circumvent the pro-rata rule. The rule looks at your aggregate IRA balances.

Common Pitfalls and Mistakes to Avoid with Multiple Roth IRAs

The Excess Contribution Nightmare

As highlighted, exceeding the annual limit across all accounts is the #1 error. It's easy to do if you're not meticulously tracking. If you contribute $7,000 to Roth IRA A in January and then, forgetting, contribute another $2,000 to Roth IRA B in December, you have a $2,000 excess. You must correct it by the tax filing deadline (including extensions). The correction involves withdrawing the excess amount plus any net income it earned. If you miss the deadline, the 6% excise tax applies each year it remains. Setting up a single master spreadsheet or using personal finance software that aggregates all investment accounts is non-negotiable for multi-account holders.

Missing the Deadline and Misunderstanding "Contribution"

IRA contributions for a given tax year can be made up until the tax filing deadline in April of the following year (e.g., for 2024, you have until April 15, 2025). This is a common source of confusion. You open a Roth IRA in February 2025 and think you're contributing for 2025, but if you don't specify the tax year, the custodian will default it to 2025. You must explicitly designate it as a 2024 contribution if you want to use your 2024 limit. When managing multiple accounts, ensure you and your custodian are on the same page for each deposit's tax year assignment.

Ignoring the Aggregation Rule for RMDs and Deductions

While Roth IRAs themselves have no Required Minimum Distributions (RMDs) for the original owner during their lifetime, the IRS aggregates all of your Traditional, SEP, and SIMPLE IRAs for RMD calculation purposes. If you have a Traditional IRA, you must calculate the RMD based on the total value of all such accounts and can satisfy it from any one or combination. This rule also applies to the deductibility of Traditional IRA contributions. If you (or your spouse) are covered by a workplace retirement plan, your ability to deduct Traditional IRA contributions depends on your MAGI and is also subject to aggregation rules across all your non-Roth IRAs. Having multiple Roth IRAs doesn't affect this, but having multiple Traditional IRAs with pre-tax money can complicate backdoor Roths and deductions.

State-Specific Nuances and creditor Protection

While federal rules are uniform, state laws differ regarding IRA creditor protection in bankruptcy or from lawsuits. Some states offer strong protection for all IRA types, including Roths, up to certain limits. Others offer less. If you are using multiple Roth IRAs for asset protection planning, you must understand your state's specific statutes. Additionally, a few states have their own estate or inheritance tax rules that could affect how inherited Roth IRAs are treated. Always consider consulting with a local estate planning attorney if these issues are a concern.

Conclusion: Your Roth IRA Blueprint for Success

So, how many Roth IRAs can you have? The definitive, liberating answer is: As many as you want. The IRS sets no ceiling on the number of Roth IRA accounts you can open and maintain. This is a feature, not a bug, granting you unparalleled flexibility to customize your retirement savings architecture. You can tailor investment platforms to specific strategies, segregate assets for different goals, and execute advanced maneuvers like the backdoor Roth with administrative clarity.

However, this freedom operates within a strict federal framework. Your single, annual contribution limit—$7,000 for those under 50, $8,000 for those 50 and older in 2024—is the immutable cap that binds all your Roth (and traditional) IRAs together. Exceeding it, even accidentally across multiple accounts, triggers costly penalties. Your ability to contribute directly at all is also gated by MAGI income limits, which for 2024 phase out between $146k-$161k for singles and $230k-$240k for married couples filing jointly.

For those above these income thresholds, the backdoor Roth IRA remains a vital, legal pathway, but one that demands careful navigation of the pro-rata rule to avoid unintended taxes. Remember the special considerations for spousal Roth IRAs, the clean separation of inherited Roth accounts, and the permanent tax-free growth that makes this vehicle so powerful. The absence of RMDs for original owners provides unmatched legacy planning flexibility.

The ultimate strategy is not about chasing a mythical maximum number of accounts. It's about intentional account structuring. Open a second or third Roth IRA only if it serves a clear purpose: better investment choices, goal-based tracking, or simplifying complex strategies. Above all, become the vigilant guardian of your annual contribution total. Use budgeting apps, maintain a master contribution log, and consider consolidating if the administrative burden outweighs the benefits. When in doubt, especially with high incomes, conversions, or inherited accounts, consult with a qualified tax advisor or financial planner. They can help you build a compliant, efficient Roth IRA ecosystem that turns the simple answer—"unlimited"—into a sophisticated engine for your tax-free retirement wealth.