Why Is Robinhood Holding My Funds? The Surprising Truth Behind Your Pending Cash

Have you ever logged into your Robinhood app, ready to make your next investment or withdraw some cash, only to see a frustrating message: "Robinhood is holding my funds"? You stare at the screen, wondering why your hard-earned money is stuck in limbo. This confusing and often anxiety-inducing situation is a common experience for many retail investors. Understanding the why behind these holds is not just about alleviating immediate frustration; it’s about becoming a more informed, empowered, and secure investor in the fast-paced world of commission-free trading. This comprehensive guide will dismantle the mystery, explaining every major reason your funds might be held, from standard industry processes to specific platform policies, and give you the actionable knowledge to navigate it effectively.

Decoding the "Hold": It's Not Personal, It's Procedural

Before diving into the specific reasons, it's crucial to shift your perspective. A "hold" on your funds is rarely a personal action taken against you. Instead, it is a standard risk management and regulatory compliance procedure embedded in the plumbing of the modern brokerage system. Robinhood, like all U.S. brokerages, operates within a strict framework set by regulators like the SEC and FINRA, and it relies on clearing firms (like Apex Clearing) to finalize transactions. These holds are automated safeguards designed to protect you, the brokerage, and the entire financial system from errors, fraud, and settlement failures. Your confusion is understandable, but the mechanism behind it is a necessary, if sometimes opaque, part of how markets function.

The Most Common Culprit: The Settlement Period (T+2)

The single most frequent reason for a hold on your recently sold stock proceeds is the settlement cycle. In the U.S., the standard settlement for stock trades is T+2, meaning "trade date plus two business days." When you sell a share on Monday (T), the transaction isn't officially final until Wednesday (T+2) at the earliest. Until that settlement is complete, the cash from the sale is considered "unsettled" and is typically restricted from being withdrawn or used to buy other securities that would themselves require settlement.

- How it works in practice: You sell 10 shares of XYZ on Tuesday. On Wednesday, your Robinhood buying power might still show the old balance because the cash from Tuesday's sale hasn't settled yet. By Thursday or Friday, the cash should become available. Robinhood often provides instant deposits and instant settlement for buying power, which can mask this process, but the underlying settlement with the clearinghouse still occurs. Attempting to withdraw unsettled funds will trigger a hold or rejection.

- Actionable Tip: Always check your "Buying Power" versus your "Cash" balance in the Robinhood app. Buying power includes unsettled funds from recent sales for immediate trading, while the cash balance only shows fully settled funds available for withdrawal. Plan withdrawals based on your settled cash balance.

Regulation T (Reg T) and Good Faith Violations

Regulation T is a Federal Reserve rule that governs the extension of credit by brokers. In simpler terms, it sets the initial margin requirements and rules around using unsettled proceeds. A Good Faith Violation (GFV) occurs when you buy a security with unsettled funds and then sell that security before the funds used for the original purchase have settled.

- The Vicious Cycle: This is a major trap for active traders. Example: You have $1,000 settled cash. On Monday, you use that $1,000 plus an additional $500 from the sale of Stock A (which hasn't settled) to buy Stock B for $1,500. On Tuesday, you sell Stock B. Because you sold Stock B before the $500 from Stock A's sale settled, you've committed a GFV. Robinhood's system will then place a 90-day restriction on your account. During this period, you can only buy securities with fully settled cash. Repeated GFVs can lead to your account being restricted to cash-only trading, which is a significant limitation.

- Why the Hold Happens: After a GFV, Robinhood effectively "holds" your buying power by restricting it to settled funds only to enforce the Reg T rules. The system is holding your ability to trade on margin (even unintentional margin) to prevent further violations.

- Statistic to Know: According to FINRA, pattern day trader accounts that incur multiple GFVs are a significant portion of margin restriction cases. Staying aware of your settlement dates is the #1 defense.

Account Security and Verification Holds

If you've recently taken an action that changes your account's fundamental status, Robinhood's compliance team may place a temporary hold for verification. This is a protective measure for your account security.

- Common Triggers:

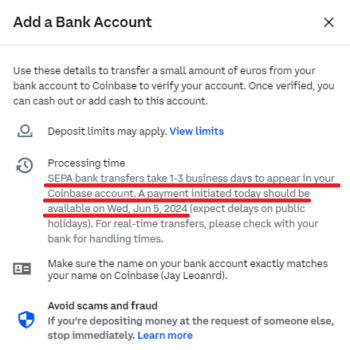

- New Bank Link: Adding a new external bank account for the first time. Robinhood may hold transfers to and from that new account for 5-7 business days while they verify the micro-deposits.

- Large Withdrawal Request: A withdrawal amount that is significantly larger than your typical pattern or that depletes your account to a very low balance may be flagged for manual review to prevent fraudulent activity.

- Suspicious Activity: Unusual login locations, rapid trading in a new account, or other behaviors that trigger their fraud detection algorithms.

- Document Submission: Uploading documents for identity verification (like a passport or utility bill) can result in a temporary hold until the review is complete.

- What to Do: Ensure your contact information (email, phone) is up-to-date so Robinhood can contact you if they need additional information. Respond promptly to any verification requests to lift the hold faster.

Payment for Order Flow (PFOF) and Market Maker Dynamics

This is a more systemic, industry-wide reason that indirectly influences holds. Robinhood's business model is heavily reliant on Payment for Order Flow (PFOF). They sell your retail order flow to high-frequency trading firms (market makers like Citadel Securities, Virtu) who execute those trades. In return, these market makers pay Robinhood a fraction of a penny per share.

- The Connection to Holds: To manage the risk of this practice and ensure they can fulfill their obligations to these market makers, Robinhood and its clearing firm (Apex) implement sophisticated risk controls. During periods of extreme market volatility (think GameStop short squeeze, meme stock rallies, or a major economic announcement), these systems become hypersensitive.

- The clearing firm may impose temporary liquidity holds on all accounts or on specific high-volatility stocks to ensure there is sufficient capital to cover potential settlement failures across millions of accounts.

- Your individual account might be flagged if your trading pattern suddenly becomes very aggressive in a volatile stock, triggering an internal risk review.

- The Bottom Line: While not a direct "hold on your funds" message, during these times, you might experience delays in access to full buying power or withdrawal availability as the entire backend system goes into a more conservative mode. A 2021 SEC report noted that PFOF arrangements can create incentives for brokers to route orders in ways that may not always achieve the best price for customers, highlighting the complex trade-offs in this model.

Margin Calls and Maintenance Requirements

If you are trading on margin (borrowed money from Robinhood), a hold can be a direct result of your account falling below maintenance margin requirements.

- How it Happens: The value of your marginable securities drops. Your equity (account value minus loan) falls below Robinhood's required maintenance margin level (often 25-30% for Reg T, but can be higher for volatile stocks). Robinhood will issue a margin call.

- The "Hold" Effect: Until you deposit sufficient cash or eligible securities to bring your account back into compliance, Robinhood may restrict your account. This restriction can manifest as an inability to withdraw funds, buy new securities (except to cover the call), or even a forced liquidation of positions to cover the deficit. The "hold" is on your account's full functionality until the financial health is restored.

- Critical Warning: Ignoring a margin call leads to a liquidation. Robinhood will sell your positions, often without notice, to repay the loan. This can happen at deeply inopportune prices, locking in significant losses.

Navigating the Hold: Your Action Plan

Seeing that hold message is the first step. The next step is taking informed action.

- Diagnose Instantly: Open your Robinhood app. Go to your account details. Look for specific notifications or banners explaining the hold. Check your "Account Statements" and "History" tabs. The reason is almost always listed there—e.g., "Funds from sale of [Stock] are pending settlement" or "Account restricted due to Good Faith Violation."

- Understand the Timeline: Is it a standard T+2 hold? That's automatic and will lift on its own. Is it a GFV restriction? That's 90 days. Is it a security verification? That depends on your response time. Knowing the type of hold tells you the duration.

- Contact Support Strategically: If the hold reason is unclear or you believe it's an error, contact Robinhood support. Do not just say "my funds are held." Be specific: "I see a restriction code XYZ on my account from [Date] due to [Reason from statement]. Can you confirm the expected release date and if any action is needed from me?" Provide transaction IDs. Be polite but persistent.

- Prevent Future Holds:

- Trade with Settled Cash: The golden rule. Use the "Cash" balance, not the "Buying Power" balance, as your guide for new purchases if you want to avoid GFVs.

- Monitor Volatility: Be extra cautious using margin or aggressive strategies during high-volatility periods. Assume holds may be longer.

- Secure Your Account: Use strong, unique passwords and 2-factor authentication to prevent security flags.

- Read the Fine Print: Familiarize yourself with Robinhood's Customer Agreement and Margin Handbook. The rules around GFVs and margin calls are spelled out there.

Frequently Asked Questions (FAQs)

Q: Can I withdraw funds that are shown as "Buying Power" but not "Cash"?

A: No. Buying Power often includes unsettled funds from recent sales or instant deposit credits. Only your "Cash" balance represents funds that have fully settled and are eligible for withdrawal. Attempting to withdraw more than your settled cash will fail and may trigger a violation.

Q: How long does a security verification hold last?

A: Typically 5-7 business days after you submit the requested documents. If you haven't submitted anything, the hold remains indefinitely. Proactively check your email and app notifications for any verification requests.

Q: Is Robinhood holding my funds because they are insolvent or in trouble?

A: Almost certainly not. Robinhood is a registered broker-dealer with the SEC and a member of FINRA and SIPC. SIPC protects customers up to $500,000 (including $250,000 for cash) if the firm fails. Isolated holds are account-specific procedural issues, not signs of a firm-wide liquidity crisis. However, during extreme market stress (like March 2020 or Jan 2021), all brokerages can experience processing delays.

Q: What's the difference between a hold and a restriction?

A: A hold typically refers to a temporary delay on a specific fund (e.g., from a sale). A restriction is a broader limitation placed on your account's trading or withdrawal privileges (e.g., a GFV restriction or margin call). Both prevent you from accessing money, but a restriction is more severe and account-wide.

Q: Does Robinhood pay interest on cash held in my account?

A: Currently, Robinhood does not offer a high-yield cash sweep program or interest on uninvested cash balances like some traditional brokers. Your cash sits in a custodial account at a partner bank, earning minimal or no interest. This is a key difference from platforms that automatically sweep cash into FDIC-insured programs.

Conclusion: Knowledge is Your Best Investment

The mystery of "why is Robinhood holding my fund" is almost always solved by understanding the three pillars of modern brokerage operations: settlement cycles, regulatory rules (like Reg T), and risk management systems. These holds are not arbitrary punishments but the necessary friction points that keep the multi-trillion-dollar trading ecosystem running smoothly and compliantly. While they can be frustrating, they are a small price to pay for the accessibility and zero-commission structure that platforms like Robinhood provide.

Your power as an investor lies in moving from confusion to comprehension. By monitoring your settled cash, respecting the T+2 timeline, avoiding good faith violations, and securing your account, you can minimize these holds entirely. When they do occur, you'll know exactly what message to look for, how long it will last, and whether you need to take action. In the end, navigating these procedural waters with confidence is a fundamental skill for any self-directed investor. It transforms a moment of frustration into a lesson in financial literacy, ensuring your capital remains as mobile and available as you intend it to be.