Debit Card Account Number Exposed: What It Is, Where To Find It, And How To Keep It Safe

Have you ever held your debit card and wondered about the string of numbers printed on it? Specifically, which one is your actual bank account number? It’s a common point of confusion, and misunderstanding this critical piece of information can have real implications for your financial security. The term "account no on debit card" often leads people to believe their primary bank account number is prominently displayed, but the reality is more nuanced—and designed to protect you. This comprehensive guide will demystify everything about the numbers on your debit card, clearly distinguishing your account number from your card number, explaining where (and if) it appears, and arming you with essential knowledge to safeguard your finances against fraud and misuse.

Understanding the anatomy of your debit card is the first step toward mastering personal finance security. While the 16-digit card number gets most of the attention during online purchases, the underlying bank account number is the true destination for your funds. Mixing these up can lead to errors in setting up direct deposits, automatic payments, or even inadvertently sharing the wrong information. By the end of this article, you’ll know exactly what your account number is, how to locate it securely, why it’s rarely printed on the card itself, and the proactive steps you must take to ensure this sensitive data never falls into the wrong hands.

What Exactly Is a Debit Card Account Number?

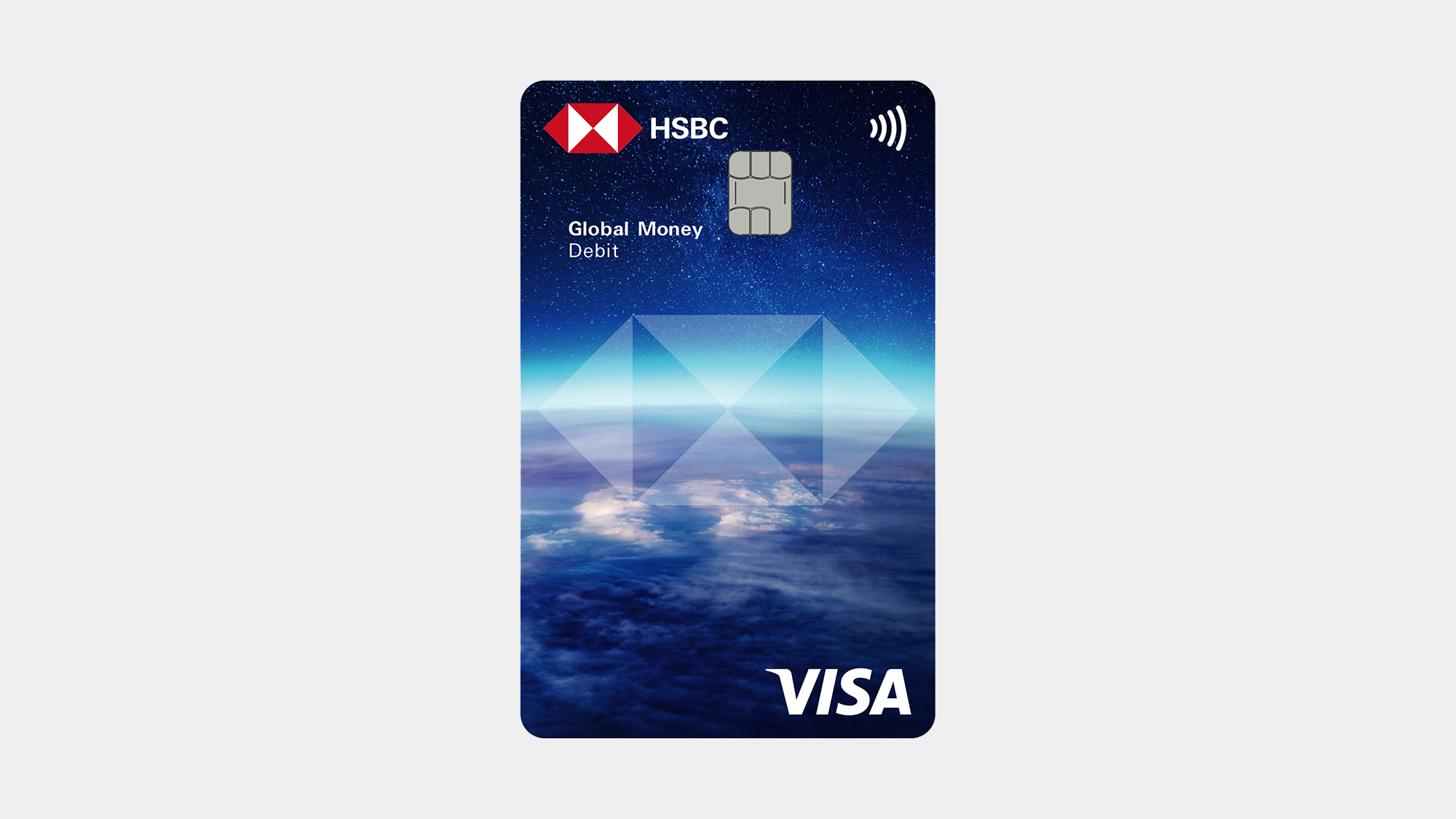

Your debit card account number is the unique identifier for your specific bank account (usually a checking or savings account) that the debit card is linked to. It’s the number your bank uses internally to route funds to and from your account. When you make a purchase or withdraw cash, the transaction network uses this number, in conjunction with other identifiers, to pull money directly from your account. Think of it as your account’s "home address" within your bank’s system. It is not the same as the 16-digit card number embossed on the front of your card, which is a separate identifier assigned by the payment network (like Visa or Mastercard) for transaction processing.

This account number is typically between 8 and 12 digits long, depending on your bank’s internal numbering system. It is part of a larger set of numbers that facilitate electronic transfers. Alongside your account number, two other critical numbers exist: the routing number (a 9-digit code identifying your bank) and the card number (the 16-digit number on your card). Together, the routing number and account number form the core information needed for ACH (Automated Clearing House) transfers, direct deposits, and automatic bill payments. The card number, while linked to your account, operates on a different layer of the payment ecosystem, often tokenized for security.

Where (and Why) You Won’t Usually Find Your Account Number on the Debit Card Itself

Contrary to what the phrase "account no on debit card" might suggest, your primary bank account number is almost never printed directly on the physical debit card. This is a fundamental security feature. Banks deliberately avoid printing the full account number on the card to minimize risk if the card is lost or stolen. If a criminal obtained your card and saw your account number, they would have a critical piece of information needed for certain types of fraud, such as setting up unauthorized ACH debits against your account.

So, where can you find your account number? It’s securely located in other places:

- Your Bank Checks: The bottom of a personal check typically contains both the routing number (the first 9 digits) and your account number (the series of digits after the routing number and before the check number).

- Your Monthly Bank Statement: Both paper and electronic statements will list your account number prominently.

- Your Online Banking Portal or Mobile App: This is the most secure and convenient method. Log in, and your account number will be displayed on the account summary page.

- By Calling Your Bank: You can verify your identity with a customer service representative and request your account number.

- At a Branch: Visiting a branch with proper identification allows a teller to provide your account number.

The physical debit card primarily displays the card number (16 digits), the card expiration date, and the CVV/CVC (the 3-digit security code on the back). These are used for card-present and card-not-present transactions. Your account number remains in a more protected layer of your banking relationship.

Debit Card Account Number vs. Card Number: Critical Differences Explained

Confusing your debit card account number with your debit card number is a frequent mistake with potentially serious consequences. Let’s break down the stark differences.

The Debit Card Number (Primary Account Number - PAN):

- Length: Typically 16 digits (sometimes 19).

- Purpose: Used to authorize card-based transactions at point-of-sale terminals, online merchants, and ATMs. It identifies the payment network (Visa, Mastercard, etc.) and your specific card within that network.

- Visibility:Always printed on the front of your card. It is also stored on the magnetic stripe and chip.

- Security: While sensitive, it is designed for transactional use. Merchants are required to follow PCI DSS (Payment Card Industry Data Security Standard) to protect this number. It can often be replaced without changing your underlying bank account.

The Bank Account Number:

- Length: Varies by bank (usually 8-12 digits).

- Purpose: Identifies your specific account at your financial institution for bank-to-bank transfers (ACH), direct deposits, and wire transfers. It points directly to your funds.

- Visibility:Never printed on the debit card itself. Found on checks, statements, and online banking.

- Security: Considered highly sensitive core banking data. Sharing this number, combined with the routing number, can allow others to initiate withdrawals from your account (though most banks have safeguards).

Analogy: Think of your bank as a large apartment building (the routing number identifies the building). Your account number is your specific apartment number within that building. Your debit card number is like a special key that lets you access the building’s amenities (shopping, ATM withdrawals) but doesn’t reveal your apartment number to the vendor. The key (card number) can be deactivated and replaced; if someone knows your apartment number (account number), they know exactly where your valuables are stored.

Is Your Debit Card Account Number a Security Risk? Understanding the Threats

The short answer is: yes, it is sensitive information, but the risk profile is specific and often misunderstood. Unlike a card number, which is used for immediate purchases, your account number alone is generally not enough for a criminal to steal money from your account. However, it is a critical component in a larger attack vector.

The primary risk associated with your account number and routing number is ACH fraud. A fraudster who has both numbers can attempt to set up an unauthorized electronic transfer (an ACH debit) from your account to theirs. This could be done by posing as you to a company that accepts bank transfers (like a utility or even a fraudulent payday lender) or by using a compromised online payment portal that allows bank account linking. While banks have fraud detection systems and typically allow you to dispute unauthorized ACH debits within 60 days, the process can be stressful and temporarily impact your available funds.

The risk increases dramatically if a criminal also has other personal information, such as your name, address, and date of birth, which are often available in data breaches. This combination can facilitate identity theft and more sophisticated account takeover attempts. Therefore, while your account number isn’t a "magic key," it is a vital piece of your financial identity puzzle that must be guarded diligently. Never share your account and routing numbers together unless you are initiating a trusted transaction (like setting up payroll direct deposit with your employer).

How to Protect Your Debit Card Account Number: Actionable Security Tips

Protecting your bank account number requires a mindset of proactive vigilance. Since it’s not on your card, the focus shifts to securing the digital and paper documents where it resides.

1. Secure Your Checkbook: Your checks are a prime source of both your routing and account numbers. Treat your checkbook like cash. Never leave it in your car or an unsecured location. When you receive new checks, store them safely. Consider using a secure checkbook cover that obscures the numbers when closed.

2. Guard Your Bank Statements: Whether paper or digital, statements contain your account number. Shred paper statements before disposal. For e-statements, ensure your email account is secured with a strong, unique password and two-factor authentication (2FA). Never email your account number.

3. Be Wary of Unsolicited Requests: Legitimate companies will rarely, if ever, call or email you asking for your full account number to "verify" your identity. If in doubt, hang up and call your bank directly using the number on the back of your card or your statement.

4. Use Strong Online Banking Hygiene: Access your online banking only on secure, private networks (avoid public Wi-Fi). Use a strong, unique password and enable 2FA. Log out after each session.

5. Monitor Your Accounts Relentlessly: The single best defense is early detection. Enroll in account alerts (via text or email) for any transaction or for low balances. Review your transactions weekly, not just monthly. Many banks offer real-time notifications through their mobile apps.

6. Be Cautious with Third-Party Payment Apps: Services like Venmo, Zelle, or PayPal require linking a bank account. Only use these with trusted individuals and reputable merchants. Understand the platform's liability policies. Once you link your account, you are sharing your account number (via tokenization) with that service.

7. Educate Yourself on Phishing Scams: Be suspicious of emails or texts claiming to be from your bank asking you to "confirm" or "update" your account details. These are often phishing attempts to steal your login credentials, which could give a criminal access to your account number and more. Never click links in unsolicited messages; go directly to your bank’s website or app.

Common Myths and Misconceptions About Account Numbers on Debit Cards

Let’s debunk some persistent myths that can lead to false security or unnecessary panic.

Myth 1: "My full account number is printed on my debit card for easy reference."

- Fact: As established, this is almost universally false. The number on your card is the card number (PAN), a separate identifier. Your bank’s customer service can confirm this.

Myth 2: "If someone has my card number, they can drain my account."

- Fact: While card number theft is serious (leading to card-not-present fraud), the card number alone typically does not grant direct access to your bank account number. Fraudulent transactions are processed against the card's credit line (which is your own money in the case of debit), but setting up new ACH debits requires the account and routing numbers. However, sophisticated fraudsters can sometimes use card numbers in social engineering attacks to trick banks into revealing more information.

Myth 3: "My account number is the same as my card number."

- Fact: They are completely different sequences of numbers with different purposes and lengths. Your account number is tied to your bank account; your card number is tied to the payment network.

Myth 4: "I need to give my account number to anyone who asks for a 'bank account number' for payment."

- Fact: Be extremely cautious. Legitimate scenarios include employers for direct deposit, the IRS for tax refunds (though they now use a secure portal), or trusted utility companies. For one-time payments, using a credit card (which offers stronger fraud liability protections) or a payment app linked to a card is often safer than providing your raw account number.

Myth 5: "My bank will cover all losses if my account number is used fraudulently."

- Fact: Under the Electronic Fund Transfer Act (EFTA), your liability for unauthorized electronic transfers (like ACH fraud) depends on how quickly you report it. If you report within 2 days, your liability is capped at $50. After 2 days but within 60 days, it can be up to $500. After 60 days, you could potentially lose the entire amount. Prompt reporting is crucial.

What to Do Immediately If You Suspect Your Account Number is Compromised

If you believe your bank account number and routing number have been exposed or used fraudulently, time is of the essence. Follow this immediate action plan:

Contact Your Bank Immediately: Call the fraud or lost/stolen card number on the back of your debit card or from your statement. Report the suspected compromise. Ask them to:

- Place a fraud alert or freeze on your account to prevent new ACH debits.

- Issue you a new debit card with a new card number (this does not change your account number but secures the card-linked transactions).

- Inquire about changing your account number. Some banks can do this for a fee, which is the most definitive way to stop ACH fraud using the old number, but it can be disruptive as you’ll need to update all automatic payments.

- Dispute any unauthorized transactions.

Monitor All Accounts Closely: Check your transaction history multiple times a day for the first week. Look for small, unfamiliar debits—fraudsters often test with tiny amounts.

File a Police Report: If you know how the information was stolen (e.g., robbery, phishing), file a report. This creates an official record.

Update Automatic Payments: If you change your account number, you must manually update every entity with your old account details (employer for direct deposit, utilities, subscription services, etc.). Your bank may provide a service to help notify some payees, but you are ultimately responsible.

Consider a Credit Freeze: While your bank account number isn’t part of your credit report, if the compromise was part of a larger identity theft, freezing your credit with the three major bureaus (Equifax, Experian, TransUnion) can prevent new lines of credit from being opened in your name.

Change Online Banking Credentials: Even if the breach wasn’t through your online account, change your password and security questions as a precaution.

The Interplay Between Routing Numbers, Account Numbers, and Your Debit Card

To fully grasp "account no on debit card," you must understand the supporting cast. Your routing number (9 digits) identifies your bank or credit union. Your account number identifies your specific account at that institution. Together, they are the ABA routing number and account number pair required for all ACH transfers, wire transfers, and setting up direct deposits/withdrawals.

Your debit card is a tool that accesses the funds in the account identified by that number. When you swipe, dip, or tap your card, the payment network communicates with your bank using the card number. Your bank then checks if the card is valid and linked to an active account in good standing, and if sufficient funds exist, it authorizes the transaction, debiting your account. The card number acts as a proxy or token for your account number during most everyday transactions. This tokenization is a key security layer—merchants see and store the card number, not your actual account number, reducing the exposure of your core banking data.

This is why, when you set up an online payment with a service like PayPal or when your employer sets up payroll, they will ask for your routing and account numbers (found on a check), not your debit card number. The card number is for the payment network; the account number is for your bank.

Frequently Asked Questions About Debit Card Account Numbers

Q: Can I find my account number by calling my bank’s automated line?

A: Often, yes. After verifying your identity through a series of security questions (e.g., recent transactions, SSN last 4 digits), the automated system may read your account number. However, speaking to a live representative is more reliable.

Q: Is it safe to give my account number for a wire transfer?

A: Wire transfers require the recipient’s routing and account numbers. If you are receiving a wire, providing your numbers is standard and safe. If you are sending a wire, you must be absolutely certain of the recipient’s details, as wire transfers are typically irreversible. Only send wires to trusted, verified entities.

Q: Why does my online banking show a different number than what’s on my checks?

A: It shouldn’t. Your account number is consistent across checks, statements, and online banking. If you see a discrepancy, contact your bank immediately, as it could indicate an error or a security issue.

Q: Do prepaid debit cards have account numbers?

A: Yes, but they are different. Prepaid cards are not linked to a traditional bank account. They have a card number and an internal account number managed by the prepaid card issuer. This number is not the same as a checking account number at a bank.

Q: What’s the difference between my account number and my member number (at a credit union)?

A: At many credit unions, your member number is your primary identifier. Your account number is often a suffix added to your member number to identify a specific account (e.g., Member #12345, Checking Account #1234501). The combined number is what you use for transactions.

Conclusion: Knowledge is Your Best Defense

The mystery surrounding the "account no on debit card" is largely by design—a security measure to keep your core banking credentials off the most commonly lost or stolen item in your wallet. Your debit card number and your bank account number serve distinct, non-interchangeable roles in the financial system. Understanding this distinction is not just trivia; it’s foundational to protecting your money.

Remember this core principle: Your bank account number is sensitive data that should be guarded with the same care as your Social Security number. It lives on your checks and statements, not your card. Never share it casually. Enroll in alerts, monitor your accounts weekly, and act immediately if you suspect any unauthorized activity. In today’s digital landscape, where data breaches are commonplace, your vigilance is the final and most critical line of defense. By internalizing these facts and adopting the protective habits outlined, you transform confusion into confidence, ensuring that your debit card remains a tool of convenient access, not a gateway for financial loss.