ACH Vs Wire Transfer: Unpacking The Key Differences That Impact Your Money

Confused about the difference between ACH and wire? You're not alone. In today's digital economy, understanding how money moves electronically is crucial for both individuals and businesses. Whether you're paying a contractor, receiving your salary, or closing on a house, the method you choose—Automated Clearing House (ACH) transfer or wire transfer—affects speed, cost, security, and even reversibility. This comprehensive guide will dissect the ACH vs wire transfer debate, providing you with the clarity needed to make informed financial decisions. By the end, you'll know exactly which tool is right for every situation.

What Exactly is an ACH Transfer?

The Automated Clearing House (ACH) network is a U.S.-based, batch-processing electronic funds transfer system governed by NACHA (The Electronic Payments Association). It's the backbone for millions of daily transactions, including direct deposits, automatic bill payments, and business-to-business payments. Think of it as a highly efficient, centralized postal service for money. Instead of sending individual messages for each transaction, ACH groups transactions together and processes them in batches at predetermined times throughout the day.

How the ACH Network Operates

An ACH transaction isn't a direct bank-to-bank transfer in real-time. It begins when an originator—like your employer or your utility company—initiates a payment request. This request is sent to their bank, the Originating Depository Financial Institution (ODFI). The ODFI bundles this request with thousands of others and submits it to an ACH Operator (the Federal Reserve or The Clearing House). The operator then sorts the batch and delivers the credit/debit instructions to the Receiving Depository Financial Institution (RDFI), which is your bank. Your bank then credits or debits your account. This entire cycle, while efficient, introduces a processing delay, which is why ACH is not instantaneous.

Common Uses of ACH Transfers

ACH is the workhorse of routine, pre-authorized payments. Its most visible form is direct deposit for payroll, tax refunds, and government benefits. For consumers, it powers recurring payments like mortgages, car loans, and subscription services (Netflix, Spotify). For businesses, it's used for supplier payments, payroll, and even person-to-person apps like Zelle (when not using its real-time feature) and Venmo (when funding via bank account). The Nacha reports that in 2023, the ACH network processed over 30 billion payments totaling more than $77 trillion, highlighting its dominance in volume.

Understanding Wire Transfers: The Express Service of Finance

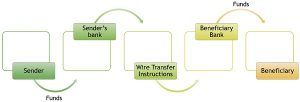

A wire transfer is a real-time, individual electronic funds transfer between financial institutions. Unlike the batch-processing ACH, a wire is a point-to-point, immediate transaction. It operates on separate, dedicated networks: Fedwire (run by the Federal Reserve) for domestic transfers and SWIFT (Society for Worldwide Interbank Financial Telecommunication) for international wires. Each wire is a unique, individually processed message sent directly from the sender's bank to the receiver's bank.

The Mechanics of a Wire Transfer

When you initiate a wire, your bank sends a secure, encrypted message containing all the details (amount, recipient's account number, routing number, etc.) over the Fedwire or SWIFT network directly to the recipient's bank. Upon validation, the recipient's bank credits the funds almost immediately, often within minutes. This direct, one-to-one communication is why wires are irrevocable once processed—the money is gone. To send a wire, you typically need the recipient's full name, bank account number, and the bank's routing number (for domestic) or SWIFT/BIC code (for international).

Typical Scenarios for Wire Transfers

Wires are reserved for high-value, time-sensitive, or one-off transactions where certainty and speed are paramount. Common examples include:

- Real Estate Closings: Down payments and closing funds.

- Large Business Transactions: Mergers, acquisitions, or major equipment purchases.

- International Remittances: Sending money abroad to family or for services.

- Legal Settlements: Court-ordered or large settlement payments.

- Investment Purchases: Funding a brokerage account for a large stock or property buy.

The Core Differences: ACH vs Wire Transfer Compared

Now, let's dive into the nitty-gritty. The difference between ACH and wire boils down to several critical factors that determine their suitability for different needs.

Speed and Timing: Days vs. Minutes

This is the most apparent difference between ACH and wire.

- ACH Transfers: Are not real-time. Standard ACH processing typically takes 1-3 business days. However, with the implementation of same-day ACH (available since 2016 and expanded over time), credits can be made available on the same business day if initiated before cutoff times. Even with same-day ACH, it's not instantaneous like a wire.

- Wire Transfers: Are designed for immediate settlement. Domestic wires via Fedwire are usually completed within minutes to a few hours, provided both banks are open and the wire is submitted before the cutoff time (often late afternoon). International wires can take 1-2 business days due to intermediary banks and different time zones, but are still vastly faster than standard ACH for cross-border payments.

Cost: Free vs. Fee

The financial difference between ACH and wire is significant.

- ACH Transfers: Are extremely low-cost, often free for consumers. Businesses may pay a small per-transaction fee (often pennies to a few dollars) or a monthly fee for bulk processing. This makes ACH ideal for high-volume, low-value payments.

- Wire Transfers: Carry substantial fees. Outgoing domestic wires typically cost $20-$50 for the sender. Incoming wires may also incur a fee for the recipient ($10-$20). International wires are even more expensive, often $40-$60 or more, plus potential intermediary bank fees and currency conversion spreads. These fees make wires impractical for small, routine payments.

Security and Irreversibility: A Critical Distinction

This is arguably the most important difference between ACH and wire regarding risk.

- ACH Transfers: Are reversible under specific circumstances. The ACH network has rules that allow for return entries if a payment was unauthorized, duplicated, or if the account is closed. This provides a safety net for consumers and businesses who send a payment by mistake or are victims of fraud. The reversal process, however, has strict timelines (typically 60 days from settlement for unauthorized debits).

- Wire Transfers: Are final and irrevocable once the funds are accepted by the recipient's bank. If you send a wire in error or to a scammer, getting the money back is extremely difficult and often impossible. Banks have no obligation to recall a wire, and if they attempt it, the recipient must voluntarily return the funds. This makes wires a prime target for wire transfer fraud and social engineering scams.

Transaction Limits and Use Case Scope

- ACH Transfers: Have limits set by individual banks and ACH rules. These can range from a few thousand dollars per day to much higher for established business accounts. They are designed for recurring, smaller-to-medium payments. The same-day ACH limit was recently increased to $1 million per transaction, broadening its use for larger business payments.

- Wire Transfers: Generally have much higher limits, often into the millions of dollars for personal and business accounts, subject to bank approval and available funds. There is no inherent network limit on the Fedwire system, making it the only viable option for multi-million dollar transactions.

International Capabilities

- ACH: Primarily a U.S.-domestic system. While there are international ACH equivalents (like SEPA in Europe), the U.S. ACH network itself does not send money abroad. To pay someone overseas via ACH-like speed and cost, you'd need a specialized international ACH service (IAT), which is not universally available.

- Wire Transfers: Are the standard for international payments. The SWIFT network connects over 11,000 financial institutions in more than 200 countries. While more expensive and complex than domestic wires, they are the global default for large, urgent cross-border transfers.

Head-to-Head: ACH vs Wire Transfer Comparison Table

| Feature | ACH Transfer | Wire Transfer |

|---|---|---|

| Network | Automated Clearing House (NACHA) | Fedwire (Domestic) / SWIFT (International) |

| Processing | Batch Processing | Real-Time, Individual Processing |

| Speed | 1-3 Business Days (Standard) / Same-Day (Available) | Minutes to Hours (Domestic) / 1-2 Days (International) |

| Cost (Sender) | Often Free (Consumers) / Low Fee (Businesses) | $20 - $60+ (Domestic) / $40 - $80+ (International) |

| Irreversibility | Reversible for errors, fraud, unauthorized debits | Final and Irrevocable once processed |

| Typical Use | Payroll, bills, subscriptions, B2B payments | Real estate, large purchases, international remittances |

| Transaction Limits | Bank-Dependent (Up to $1M for same-day ACH) | Very High (Often Millions, subject to bank) |

| International | No (U.S. domestic only) | Yes (Primary method via SWIFT) |

Practical Examples: When to Use Which?

Understanding the difference between ach and wire is useless without application. Here’s how to choose in real-world scenarios.

Choose ACH When:

- You are setting up recurring payments (rent, utilities, gym membership).

- Your employer is depositing your paycheck.

- You are a business paying multiple vendors or employees monthly.

- You want to send money to a friend or family member with no rush (using services like Zelle within bank limits, or standard bank transfers).

- Cost is a primary concern and the transaction is not time-sensitive.

- You desire the protection of reversibility in case of a mistake.

Choose a Wire When:

- You are closing on a home and need to fund the down payment and closing costs by a specific, imminent deadline.

- You are making a large, one-time business payment for an asset or acquisition.

- You are sending urgent funds internationally to a family member in need.

- The recipient requires a wire (common in real estate and some B2B contracts).

- You need proof of immediate, cleared funds for a transaction.

- The transaction value is so high that the wire fee is a negligible cost for the speed and certainty.

Addressing Common Questions and Concerns

Is ACH Safe?

Yes, ACH is very safe. It operates under strict NACHA rules and Regulation E (for consumer protections). The reversibility feature is a key safety net. However, you must safeguard your bank account details. Fraudulent ACH debits can be disputed, but you must report them promptly.

Can a Wire Be Traced?

Yes, wires can be traced. Each wire has a unique Fedwire reference number or SWIFT MT103 message that your bank can use to track the payment's path through the network. However, tracing does not guarantee recovery of funds if they've been withdrawn by a scammer.

What About Scams? Which is Riskier?

Wire transfers are far riskier for scams. Because they are irrevocable, they are the preferred method for fraudsters in romance scams, fake investment schemes, and business email compromise (BEC). Never wire money to someone you haven't met in person or for a deal that seems too good to be true. ACH, with its reversal window, offers a critical layer of consumer protection against unauthorized debits.

Do I Need a Routing and Account Number for Both?

Yes, for both ACH and domestic wires, you need the recipient's bank routing number and account number. For international wires, you need the recipient's IBAN (in many countries) and the bank's SWIFT/BIC code instead of a routing number.

Are There Alternatives?

Yes! The landscape is evolving. Real-Time Payments (RTP) and The Clearing House's RTP network offer instant, irrevocable, low-cost payments 24/7/365, blending some benefits of both. Third-party apps (PayPal, Venmo, Cash App) often use ACH for funding but offer instant peer-to-peer transfers within their networks. Zelle is unique as it's integrated into many banking apps and can facilitate near-instant transfers between enrolled users using just an email or phone number, often at no cost.

The Bottom Line: Mastering Your Money Movement

The fundamental difference between ACH and wire comes down to a classic trade-off: cost and reversibility versus speed and finality. ACH is your reliable, economical, and reversible workhorse for the vast majority of everyday and business payments. It powers the recurring financial commitments that keep our personal and economic lives running smoothly. Wire transfer is your express, high-stakes courier for moments when time is money and the transaction is too large or critical to leave to chance.

Your financial literacy is your best defense and tool. Before you hit "send," ask: Is this payment recurring? How time-sensitive is it? What's the dollar amount? Does the recipient explicitly require a wire? Can I afford to lose this money if it's a scam? The answers will almost always point you clearly toward ACH or wire. In an age of sophisticated financial fraud, choosing the wrong method can be catastrophic. By understanding these core differences, you move from being a passive participant in the financial system to an active, empowered manager of your own money.

Final Pro-Tip: For businesses, establishing clear policies on when to use ACH vs. wire is essential for fraud prevention and cash flow management. For individuals, always verify wire instructions in person or via a known, trusted phone number—never solely from an email, which could be compromised. When in doubt, call your bank. A few minutes of verification can save you from a permanent, devastating financial loss.

:max_bytes(150000):strip_icc()/ach-vs-wire-transfer-3886077-v3-5bc4cc6d4cedfd0051485d64.png)