Understanding Chapter 13 Bankruptcy: A Comprehensive Guide To Debt Repayment Plans

Are you drowning in debt and wondering if there's a lifeline? Chapter 13 bankruptcy might be the solution you've been searching for. But how does bankruptcy Chapter 13 work exactly? This comprehensive guide will walk you through the entire process, helping you understand whether this debt relief option is right for your financial situation.

What is Chapter 13 Bankruptcy?

Chapter 13 bankruptcy, often called the "wage earner's plan," is a type of bankruptcy that allows individuals with regular income to develop a plan to repay all or part of their debts over three to five years. Unlike Chapter 7 bankruptcy, which liquidates assets to pay creditors, Chapter 13 enables you to keep your property while catching up on overdue payments.

The process is designed for people who have a steady income but are struggling with overwhelming debt. It provides a structured way to reorganize finances and create a manageable repayment plan that fits within your budget. According to the United States Courts, approximately 30% of all non-business bankruptcy filings are Chapter 13 cases, making it a popular option for those seeking debt relief while maintaining their assets.

How Does Bankruptcy Chapter 13 Work? The Basic Process

The Chapter 13 process begins when you file a petition with the bankruptcy court. This petition includes detailed information about your finances, including your income, debts, assets, and expenses. You'll also need to submit a repayment plan that outlines how you intend to pay back your creditors over the next three to five years.

Once your petition is filed, an automatic stay goes into effect, immediately stopping most collection actions against you. This means creditors must cease harassing phone calls, wage garnishments, and foreclosure proceedings. The court then appoints a bankruptcy trustee to oversee your case and distribute payments to your creditors according to your proposed plan.

After filing, you'll attend a meeting of creditors where your trustee and any interested creditors can ask questions about your financial situation and proposed plan. If the court approves your plan, you'll make monthly payments to the trustee for the duration of the plan. These payments are then distributed to your creditors based on the terms you've established.

Eligibility Requirements for Chapter 13 Bankruptcy

Not everyone qualifies for Chapter 13 bankruptcy. To be eligible, you must have unsecured debts less than $419,275 and secured debts under $1,257,850 (these figures are adjusted periodically for inflation). You must also have a regular source of income and be an individual, not a business entity.

Additionally, you cannot have filed for bankruptcy in the previous 180 days if your case was dismissed for certain reasons, such as failing to appear in court or comply with court orders. You must also complete credit counseling from an approved agency within 180 days before filing your case.

Creating Your Chapter 13 Repayment Plan

The heart of Chapter 13 bankruptcy is your repayment plan. This document details how you'll pay back your creditors over the life of your bankruptcy. Your plan must commit all of your disposable income for the duration of the plan period and must be completed within 3-5 years.

Your plan is based on several factors, including your income, expenses, and the types of debt you have. Priority debts like recent taxes and domestic support obligations must be paid in full. Secured debts like mortgages and car loans may be modified or paid through the plan. Unsecured debts like credit cards and medical bills typically receive only a percentage of what's owed, often pennies on the dollar.

The court will review your plan to ensure it meets all legal requirements and is feasible based on your income and expenses. Your creditors will also have an opportunity to object to your plan if they believe it doesn't adequately address their claims.

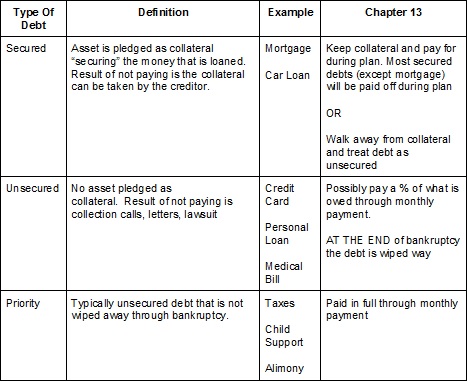

Types of Debts in Chapter 13 Bankruptcy

Understanding the different types of debts is crucial when considering Chapter 13 bankruptcy. Secured debts are those backed by collateral, such as your home or car. In Chapter 13, you may be able to catch up on missed payments and keep the property.

Unsecured debts don't have collateral backing them. These include credit card debt, medical bills, and personal loans. In Chapter 13, these debts are often paid a percentage of what's owed, with the remainder discharged at the end of your plan.

Priority debts are certain obligations that must be paid in full through your bankruptcy plan. These include most tax debts, domestic support obligations, and wages you owe to employees. Understanding how each type of debt is treated can help you create a realistic repayment plan.

The Role of the Bankruptcy Trustee

The bankruptcy trustee plays a crucial role in your Chapter 13 case. This court-appointed official reviews your petition and proposed plan, conducts the meeting of creditors, and distributes payments to your creditors throughout your plan period.

The trustee also monitors your case to ensure you're complying with the terms of your plan. If you miss payments or experience a significant change in your financial situation, the trustee may recommend that your case be dismissed. Working cooperatively with your trustee is essential for successfully completing your Chapter 13 bankruptcy.

Completing Your Chapter 13 Plan Successfully

Successfully completing your Chapter 13 plan requires dedication and careful financial management. You'll need to make all required monthly payments to the trustee on time. If you experience financial difficulties during your plan, it's crucial to communicate with your trustee immediately rather than simply missing payments.

Many people struggle with maintaining their plan payments, especially if they experience job loss or unexpected expenses. However, the bankruptcy code does provide some flexibility. You may be able to modify your plan if your circumstances change significantly, or even convert to Chapter 7 bankruptcy if necessary.

Once you've made all required payments under your plan, you'll receive a discharge of any remaining eligible debts. This discharge is a powerful benefit of Chapter 13 bankruptcy, allowing you to emerge from bankruptcy with a fresh financial start.

Chapter 13 vs. Chapter 7: Which is Right for You?

When considering bankruptcy options, many people wonder whether Chapter 13 or Chapter 7 is the better choice. Chapter 7 bankruptcy is a liquidation bankruptcy that typically takes only a few months to complete. It's often chosen by those with limited income who don't want to repay their debts.

Chapter 13, on the other hand, takes several years to complete but allows you to keep your assets and repay debts according to a structured plan. It's often the better choice if you're behind on mortgage or car payments and want to catch up without losing your property.

The right choice depends on your specific financial situation, including your income, assets, and types of debt. Consulting with a qualified bankruptcy attorney can help you determine which option is best for your circumstances.

Common Misconceptions About Chapter 13 Bankruptcy

Many people have misconceptions about Chapter 13 bankruptcy that can prevent them from considering it as an option. One common myth is that bankruptcy will ruin your credit forever. While bankruptcy does impact your credit score, you can begin rebuilding your credit immediately after your case is complete.

Another misconception is that you'll lose everything you own in bankruptcy. In reality, Chapter 13 allows you to keep your assets while repaying your debts. You may even be able to reduce certain secured debts through a process called "cramdown."

Some people also believe that only "irresponsible" people file for bankruptcy. However, many individuals who file for bankruptcy have experienced job loss, medical emergencies, or other circumstances beyond their control that led to financial difficulties.

Life After Chapter 13 Bankruptcy

Completing Chapter 13 bankruptcy is a significant accomplishment that provides a fresh financial start. After receiving your discharge, you'll be free from personal liability for many of your debts. However, some obligations like student loans, certain taxes, and domestic support obligations typically cannot be discharged.

The bankruptcy will remain on your credit report for up to 10 years, but its impact on your credit score diminishes over time. Many people find that they can qualify for credit cards, car loans, and even mortgages within a few years of completing bankruptcy, often at better terms than before filing.

To make the most of your fresh start, it's important to develop good financial habits. This might include creating a budget, building an emergency fund, and using credit responsibly. Many people who complete Chapter 13 bankruptcy report feeling more financially secure and in control of their money than before filing.

Conclusion

Understanding how bankruptcy Chapter 13 works is the first step in determining whether it's the right solution for your financial challenges. This powerful tool offers a structured way to repay debts while keeping your assets, providing a path to financial recovery that simply isn't available through other means.

While the process requires commitment and careful financial management over several years, the benefits can be life-changing. From stopping foreclosure proceedings to discharging remaining eligible debts at the end of your plan, Chapter 13 bankruptcy provides a comprehensive solution for those struggling with overwhelming debt.

If you're considering Chapter 13 bankruptcy, it's important to consult with a qualified bankruptcy attorney who can evaluate your specific situation and guide you through the process. With the right information and professional guidance, you can make an informed decision about whether Chapter 13 bankruptcy is the right path to your financial fresh start.