How Many Life Insurance Policies Can I Have? Unlocking The Truth About Coverage Limits

Have you ever wondered, "How many life insurance policies can I have?" It’s a question that often pops up when you’re planning for your family’s future, thinking about business succession, or just trying to get a handle on your financial safety net. The immediate assumption for many is that there’s a strict legal limit—maybe one, maybe three—set in stone by insurance regulators. But what if the real answer is far more flexible and tailored to your unique life? The truth is, there is no federal or state law that caps the number of life insurance policies an individual can own. The practical limit isn't a number on a statute book; it's a calculation based on your insurable interest, your financial need, and the underwriting approval of insurance companies. This guide will dismantle the myths, walk you through the real-world considerations, and empower you to structure a coverage plan that’s as dynamic as your life.

The Short Answer: There Is No Legal Limit, But There Are Practical Boundaries

Let’s start with the foundational truth: from a regulatory standpoint, you can apply for and own as many life insurance policies as you can get approved for. An individual could theoretically hold ten, twenty, or even fifty policies from various insurers. However, this theoretical freedom runs headfirst into the practical realities of life insurance underwriting. Insurance companies are in the business of managing risk, not writing policies willy-nilly. They must determine if you have a legitimate insurable interest in your own life (which you always do) and, more critically, whether the total amount of coverage you’re seeking across all policies is justifiable based on your income, assets, and financial obligations.

This is where the concept of "human life value" comes into play. Insurers assess what your life is financially worth to your dependents or business partners. They look at your salary, potential future earnings, debts, mortgage balances, children’s education costs, and business valuation. The total death benefit from all your policies combined should generally not vastly exceed this calculated value. If you apply for $10 million in coverage with a $200,000 annual salary and no business ownership, an insurer will rightfully question the need. Over-insurance is a red flag that can lead to denied applications or, worse, allegations of fraud if a claim is ever paid.

Understanding Insurable Interest and Underwriting Scrutiny

Insurable interest is the legal requirement that you must suffer a genuine financial loss upon the death of the insured. For your own life, you inherently have an unlimited insurable interest. The underwriting scrutiny, therefore, shifts to financial justification. When you apply for a new policy, the application will ask if you have other life insurance in force. This isn't just small talk; it’s a critical part of the needs analysis.

- The "Total Coverage" Question: Insurers will sum up all your existing policies and the new one you’re applying for. They use guidelines, often called "accumulation limits," which vary by company but typically suggest total coverage shouldn't exceed 10-20 times your annual income, or a amount that replaces your lifetime earnings potential. A business owner’s limit might be tied to their share of the company’s value.

- The Medical Information Bureau (MIB): Almost all insurers check the MIB, a database that tracks previous life insurance applications. If you have multiple recent applications or policies, it will be visible. This helps prevent "rate evasion" (hiding health issues by applying to multiple companies) and flags potential over-insurance.

- The "Staging" Concern: Applying for several policies in a short period, especially after a health event, can look like you’re trying to secure coverage before a known prognosis worsens. This can trigger deeper investigation or denials.

Strategic Reasons for Holding Multiple Life Insurance Policies

Given the scrutiny, why would anyone want more than one policy? The answer lies in strategic financial planning. Multiple policies are not about gaming the system; they’re about creating a layered, flexible, and efficient coverage structure that adapts to life’s changes.

1. The "Ladder" Strategy: Matching Coverage to Changing Needs

Your need for life insurance is not static. It’s highest when you have young children and a large mortgage, and it decreases as debts are paid and retirement savings grow. A life insurance ladder uses multiple term policies with different expiration dates (e.g., 10-year, 20-year, 30-year terms) to match this declining need.

- Example: A 35-year-old with a newborn and a $400,000 mortgage might buy:

- A $500,000 30-year term to cover income replacement until retirement.

- A $300,000 20-year term to specifically cover the mortgage period.

- A $200,000 10-year term for high-cost early childhood years.

As the shorter-term policies expire, the need diminishes, and the total premium outlay is often lower than a single, massive permanent policy. This is a cost-effective, needs-based approach.

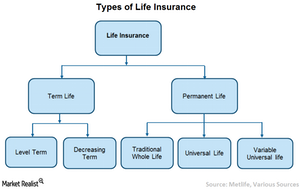

2. Blending Term and Permanent Insurance for Different Goals

Term life insurance is pure protection for a set period. Permanent life insurance (whole, universal) builds cash value and lasts for life. Using both serves distinct purposes.

- Term for Income Replacement: Use a large term policy to replace your salary for your working years.

- Permanent for Legacy & Liquidity: Use a smaller permanent policy to leave a tax-free inheritance, cover final expenses, or provide funds for estate taxes or a business buy-sell agreement. The cash value can also be accessed via policy loans for emergencies or retirement supplement.

- Example: A professional might have a $2 million 20-year term policy and a $500,000 indexed universal life (IUL) policy. The term covers the family’s lifestyle. The IUL builds cash value to fund a child’s education or supplement retirement, with a death benefit that grows over time.

3. Business Applications: Key Person, Buy-Sell, and Split-Dollar

Business owners often use multiple policies with different owners/beneficiaries to solve complex problems.

- Key Person Insurance: The business owns a policy on a crucial owner/employee, with the business as the beneficiary. This protects the company from financial loss if that person dies.

- Buy-Sell Agreements: Each partner owns a policy on the other partners, with the policy owned by the business or the individual partners. The death benefit funds the purchase of the deceased partner’s share from their estate.

- Split-Dollar Arrangements: An employer pays the premium on an employee’s policy, sharing the death benefit or cash value. This is a sophisticated executive benefit.

In these cases, one individual might be insured under 3-4 different policies, each with a different owner and beneficiary, all perfectly legitimate and necessary for the business continuity plan.

4. Maximizing Riders and Features Across Carriers

Different insurers have different strengths. One company might offer an exceptional chronic illness rider for long-term care, another might have a superior disability waiver of premium, and a third might offer a unique investment-linked index for cash value growth. By using multiple carriers, you can "shop the riders" to build a customized product suite that no single insurer can match.

5. Guaranteed Issue and Final Expense Policies

It’s common for seniors to hold a small guaranteed issue whole life policy (often $5,000-$25,000) to cover funeral costs, alongside a larger term or permanent policy from earlier in life. These small policies have no medical exam and are owned directly by the individual for final expense planning.

The Underwriting Gauntlet: How Insurers View Your Portfolio

When you apply for a new policy and disclose existing coverage, the insurer’s underwriter will perform a "needs analysis" or "financial underwriting." They are looking for consistency and reasonableness.

They will ask for:

- Copies of existing policy illustrations or declarations.

- Your most recent tax returns (often 2-3 years).

- Pay stubs or business financial statements.

- A detailed list of your assets and liabilities.

What they are trying to prevent:

- Over-Insurance: Coverage that far exceeds any conceivable financial loss.

- Stranger-Originated Life Insurance (STOLI): Schemes where investors induce seniors to take out policies they don’t need, with the investor as the beneficiary. This is illegal and fraudulent.

- Rate Evasion: Hiding pre-existing conditions by applying to multiple companies simultaneously.

A red flag example: An applicant with a $150,000 salary applies for a new $5 million term policy and already has two existing policies totaling $3 million. The total $8 million is likely unjustifiable unless the applicant is a high-earning business owner with a company valued at $20 million+. The application would probably be declined or require extreme documentation.

How to Structure Multiple Policies Correctly: A Step-by-Step Guide

If you’ve determined that multiple policies make sense, structure is everything.

Step 1: Conduct a Full Financial Needs Analysis.

Before talking to any agent, list your assets, debts, income, and future obligations (college, retirement). Calculate your human life value. This is your starting point for total coverage.

Step 2: Map Policies to Specific Goals.

Create a chart. Column A: Goal (e.g., "Pay off mortgage," "Fund child's college," "Replace income until age 65," "Leave $500k inheritance"). Column B: Policy Type (Term 20yr, IUL, Whole Life). Column C: Desired Death Benefit. Column D: Target Expiration or Cash Value Timeline.

Step 3: Shop Strategically, Not Randomly.

Don’t apply to five companies at once hoping one sticks. Work with an independent insurance agent or broker who represents multiple carriers. They can match your health profile and goals to the most suitable company’s underwriting guidelines and product strengths. A good agent will help you sequence applications to avoid raising red flags.

Step 4: Be Transparent and Organized.

On every application, fully and accurately disclose all existing insurance. Have your policy documents organized. Explain the why behind your multiple-policy strategy to the underwriter in a cover letter if necessary. For example: "Policy A is a 20-year term for mortgage protection. Policy B is a 30-year term for income replacement until retirement. Policy C is a permanent policy for estate liquidity."

Step 5: Review and Consolidate Periodically.

Life changes. Every 3-5 years, review your coverage. You might drop a term policy that’s no longer needed. You might convert a term to permanent. You might consolidate two small permanent policies into one larger one for better fee structure. Your portfolio should evolve with you.

Common Questions and Misconceptions

Q: Can having multiple policies hurt my beneficiaries?

A: No. Each policy names its own beneficiary(ies). The proceeds are paid separately and are generally income tax-free. There is no limit on how much a beneficiary can receive.

Q: What about the "Free Look" period? Can I cancel policies I don’t want?

A: Yes. Every state has a "free look" period (usually 10-30 days) after you receive the policy where you can cancel for a full refund. This is useful if you applied for multiple policies and decide you only need one or two.

Q: Do I have to tell a new insurer about my old policies?

A: Absolutely yes. It is fraud to omit material information on an insurance application. The MIB will almost certainly reveal it. Always disclose.

Q: Is it cheaper to have one big policy or multiple smaller ones?

A: It depends. A single large term policy is often the simplest and cheapest pure protection. However, a ladder strategy of smaller term policies can be cheaper overall if your need declines. Blending term and permanent is usually more expensive than term alone but provides lifelong benefits. The cost analysis must be done per your specific goals.

Q: Can I name different beneficiaries on different policies?

A: Yes, and this is a common and powerful planning tool. You can name your spouse on one, a child on another, and a trust on a third to control distribution.

The Bottom Line: Quality Over Quantity

So, how many life insurance policies can you have? As many as you can justify, get approved for, and afford to maintain. The goal is not to collect policies like trading cards. The goal is to build a comprehensive financial shield that is:

- Adequate: Covers all your identified needs.

- Appropriate: Uses the right type of insurance (term vs. permanent) for each need.

- Affordable: Premiums fit sustainably into your budget.

- Efficient: Structured to minimize costs and maximize benefits over time.

For the vast majority of families, one well-structured term policy and perhaps one small permanent policy is sufficient. For business owners, high-net-worth individuals, or those with complex estate plans, 2-4 policies might be the optimal solution. Ten or more policies would be highly unusual and would require an exceptionally complex financial picture and an experienced advisor to implement correctly.

Before you apply for another policy, pause and consult with a fee-only financial planner or a knowledgeable independent insurance agent. Bring all your existing policies. Have them run a fresh needs analysis. The answer to "how many" should come from that analysis, not from a desire to simply have more. Your life insurance portfolio should be a deliberate, strategic component of your overall financial plan—not a collection of disconnected products. By understanding the principles of insurable interest, underwriting justification, and strategic layering, you can confidently answer that initial question for yourself and build a legacy of protection that truly lasts.